Nvidia and the other US titans of tech remain engulfed in turmoil, despite the pause on ‘reciprocal’ tariffs.

But, on social media this week, Sundar Pichai, chief executive of Google parent company Alphabet, was sounding off – not about the trade war, but about his company’s new artificial intelligence (AI) system that makes dolphin language intelligible to humans.

This may have been an implicit message to investors that they should focus on the profits from AI – and look beyond the implications of Trump’s policies for the fortunes of Alphabet, as well as those of Amazon, Apple, Meta, Microsoft, Nvidia and Tesla, the rest of tech’s Magnificent Seven.

Yet it is more likely that many investors will this Easter weekend be wondering whether to say goodbye to the ‘Mag Seven’ and other US shares.

The mercurial nature of the US President’s pronouncements has produced deep uncertainty. The latest Bank of America survey shows that global fund managers are trimming back the US element of their portfolios. Jerome Powell, chairman of the Federal Reserve, the US central bank, thinks that the States could face higher inflation and lower growth.

But should you be breaking up with America? Or is it better to conclude that this should be a lasting relationship, although less lucrative than in the past? Here is what you need to know.

Is it time to wave goodbye to the US tech titans? Pictured (from left): Alphbet’s boss Sundar Pichai, Amazon’s Jeff Bezos, Apple’s Tim Cook, Meta’s Mark Zuckerberg, Microsoft’s Satya Nadella, Nvidia’s Jensen Huang and Tesla’s Elon Musk

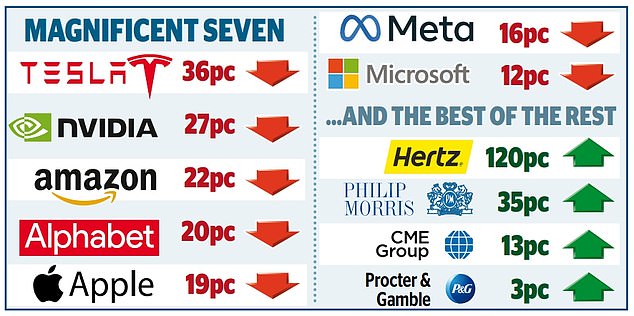

The Magnificent Seven have all seen their shares plummet over the last year – but some other companies have coped through the storm of Trump’s tariffs

The background

High anxiety gripped the market again this week with the news that the semiconductor giant Nvidia is barred from selling its chips to China, which could cost it about 10pc of its sales. Big Tech, it seems, should not expect special treatment from Trump, although its bosses are his most prominent allies.

Alarming bond market signals caused Trump to pause the tariffs. But for the time being, he is less bothered about Wall Street than Main Street, focusing on rebuilding America’s manufacturing base. In the 1950s, manufacturing jobs accounted for about 35pc of private sector employment. Today it is about 9.4pc. A weaker dollar would make US exports more attractive, which is why Trump seems to see the greenback’s status as the world’s reserve currency as a burden not a privilege.

Jane Fraser, chief executive of Citigroup, contends that, once the volatility has dissipated, ‘America will still be the world’s leading economy’

As James Harries and Tomasz Boniek, managers of the STS Global Income & Growth trust, point out, Trump’s stance on trade, the dollar and much else represents ‘a seismic shift of direction, if seen through to conclusion’.

Some US bank bosses have voiced concern. But Jane Fraser, the Scottish-born chief executive of Citigroup, contends that, once the volatility has dissipated, ‘America will still be the world’s leading economy’.

Against this background, the S&P 500 has fallen by 10pc this year to 5275. The index hit a record of 6144 in February, but the shock tariff revelations brought steep declines.

Most Wall Street strategists expect the S&P to recover in 2025, but they have lowered their year-end estimates.

Duncan Lamont of asset manager Schroders says: ‘Selling out when the Vix started to rise and returning thereafter would be a mistake’

The average target is 6067, although JP Morgan Chase is less sanguine and predicts 5200. As a consequence, even more attention will be paid to the Vix index (known as the ‘Fear Index’), a measure of how volatile traders expect the S&P to be. A Vix index of above 33 indicates alarm. The long-term average is 19. But while it may be tempting to flee when the Vix peaks, you could lose out.

Duncan Lamont of asset manager Schroders says: ‘Selling out when the Vix started to rise and returning thereafter would be even more of a mistake.

‘This strategy would have left you with $782 in 2024 if you had invested $100 in 1990, but $2895 if you had stayed put.’

The way ahead

Ian Lance of the Temple Bar investment trust argues that US shares still look overvalued.

He says: ‘In the long run, I believe, the best guide to future returns is valuation and on some measures the US market is more expensive than it was in 1929 and 2000 – and we all know what happened after that!’ Others are more optimistic. Rob Burgeman, of wealth manager RBC Brewin Dolphin, says: ‘US corporations have shown over many decades an ability to innovate and to respond rapidly to changes in the global economy.’

Peter McLean, of investment manager Stonehage Fleming, is also confident but adds: ‘Investors will need to be more discerning about valuations, sentiment and competition than in the recent past.’

Ian Lance says that in some ways ‘the US market is more expensive than it was in 1929 and 2000 – and we all know what happened after that!’

This means that it makes sense to look beyond the Mag Seven. Activist investor Bill Ackman, manager of Pershing Square, has led this way, snapping up a slice of the car rental firm Hertz.

Matthew Page, manager of the Guinness Global Equity Income fund, argues that consumer staple companies like Procter & Gamble should be able to pass on price increases if tariffs push up inflation. He also highlights CME Group, a financial services business which is benefiting from market volatility produced by Trump’s social media content and Oval Office speeches. STS Global Growth & Income holds the tobacco giant Philip Morris. Diversification into such stocks may be useful if you are overly exposed to the Mag Seven.

US stocks make up about 70pc of the global market indices. As a result, many global funds are, in reality, American funds.

Tech’s future

If you are convinced that you can live with the unpredictability of the Trump regime, most of the Magnificent Seven should deserve a place in your portfolio.

However, it is wise to lower your expectations about sales and profits. Even before the tariff crisis, it was becoming clear that these companies’ competitive edge could be eroded by new cheaper products from the Far East. For example, China’s DeepSeek AI is a rival to Silicon Valley’s expensive Chat GPT generative AI system.

But Page argues that Microsoft offers a ‘degree of defensiveness, thanks to the recurring revenues from its services and software’.

Meanwhile, despite its woes, Nvidia continues to be rated a ‘buy’ because of the quality of its AI chips, although analysts are trimming their target prices. The average is $160, against the current $102. Tesla shares will be supported by the shareholder fan base of its boss Elon Musk. Yet other investors should note that the company will not be protected from tariffs, despite Musk’s close links with the White House.

Despite its recent dip, Tesla shares will continue to be supported by the shareholder fan base of its boss Elon Musk

Abandoning tech altogether would be short-sighted, according to Helen Steers and Charlotte Morris, managers of Pantheon International trust: ‘The one thing we’re certain about is that tech is an enduring need globally – and volatility can present compelling opportunities.’

But they stress that it is vital in this environment to evaluate companies in terms of their strengths and long-term potential.

One person likely to be doing just that in tech and other industries is the legendary US investor Warren Buffett, whose Berkshire Hathaway fund is sitting on a $334bn pile of cash.

The fund’s Apple holding has been reduced but remains the largest stake, despite the corporation’s Far East supply chain.

For the moment, electronic goods, such as Apple’s iPhone, are exempt from the ‘reciprocal’ tariffs. This may be temporary, but Buffett is evidently persuaded that America’s entrepreneurial spirit has not been extinguished.

This is a reasonable bet – but one that is best balanced with bets on Europe and the UK.

As Dan Boardman-Weston, chief executive of BRI Wealth Management, argues: America has produced the richest returns over the past decade, but this may not be the case over the next decade.

Some links in this article may be affiliate links. If you click on them we may earn a small commission. That helps us fund This Is Money, and keep it free to use. We do not write articles to promote products. We do not allow any commercial relationship to affect our editorial independence.