WE all work hard for our cash, and most of us could probably do with a bit more of it in our pockets.

But there’s one way that infuriates me as many of us are accidentally throwing it away through sheer laziness – and it’s SO easy to avoid.

4

One of the biggest crisis facing finances for my generation (those in their 20s) is undoubtedly sticking with what we know when it comes to our finances.

It’s easy, isn’t it?

Your bank offers you insurance, a mortgage, or a savings account.

You’ve been with them for years. They seem trustworthy. So, you just say “yes”. Job done.

But here’s the truth: loyalty rarely pays when it comes to money. In fact, it often costs you – and it could end up making you £100s poorer each year.

When did you last shop around for your car insurance? Your home insurance? Your mortgage? Your savings or investment platforms?

If the answer is “years ago,” or even worse, “never,” you’re almost certainly paying too much.

As Chief Consumer Reporter for The Sun my email inbox is regularly pumped full of press releases from financial firms and government departments telling me that people are missing out on cash.

To make matters worse, banks and other financial institutions rely on our laziness.

They know that most of us can’t be bothered to switch.

It feels like a hassle.

There’s paperwork, phone calls, comparisons…

But honestly, in today’s world, it’s easier than ever.

Is comfort costing you

The costs can quickly add up. I’m moving home this week – so, checking my bills is top of my agenda.

For example, I bank with HSBC, and I asked them for a quote on insuring a typical three-bedroom semi-detached house, it would cost £489 per year.

But just five minutes spent adding my details into Money Supermarket I’m given a policy with the same cover for just £236 a year.

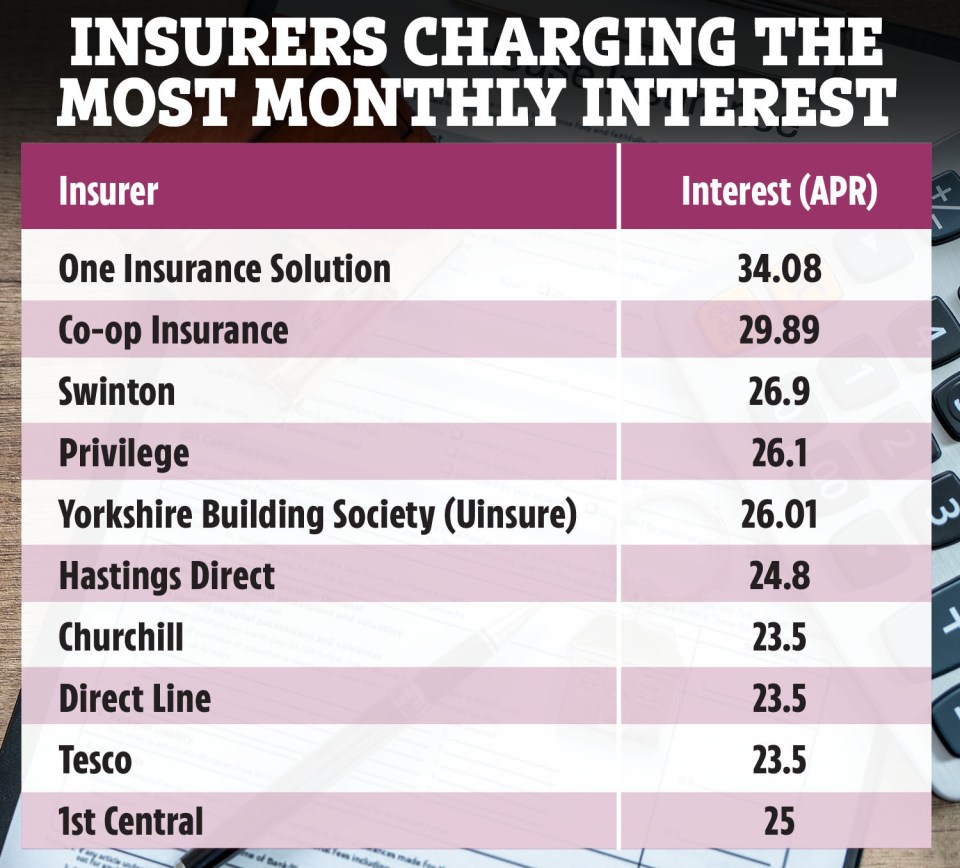

And remember the golden rule when it comes to paying for insurance – always pay annually upfront if you can.

It’s almost always cheaper than opting for monthly payments, as you’ll avoid the added interest charges that come with instalment plans.

4

The same goes with other financial products, such a mortgages.

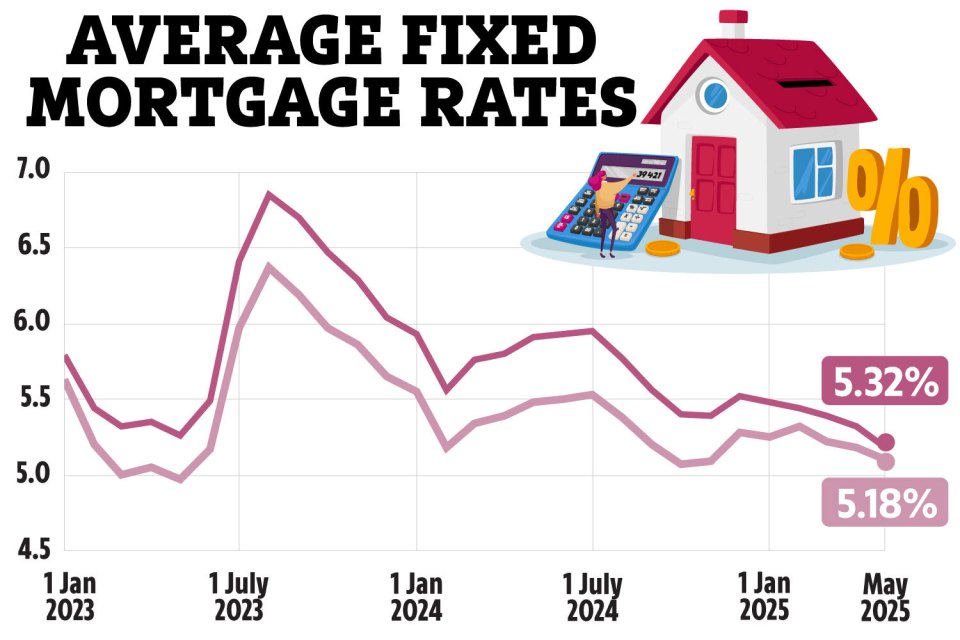

For example, if you bank with NatWest and wanted to borrow £250,000 with a 10% deposit on the open market, you’d be offered a 4.7% two-year fixed rate.

In comparison, opting for Lloyds Bank’s deal for the same loan would provide you with a more competitive rate of 4.32%.

And it all adds up – that’s a saving of £1,143 in the first two years of your mortgage.

However, to get the most competitive mortgage rates, speak to a broker who has access to whole of market deals.

Some rates are available from as low as 3.72%.

Some will charge an extra fee but there are plenty who give advice for free and get paid only on commission from the lender.

You can find local brokers through your estate agent, word of mouth or online.

Make sure the broker is a qualified mortgage adviser – the most common qualification is called CeMAP.

4

That monthly pay cheque hitting your account? A great feeling, isn’t it?

But if you’re not actively managing the money you don’t spend, your inaction could be diminishing its potential for growth.

Experts at AJ Bell recently revealed a staggering statistic – £280billion is languishing in current accounts, earning absolutely no interest.

And even if you do have a linked savings account with your high street bank, you’re unlikely to see much of a return.

According to TotallyMoney, the average easy-access account (allowing unlimited withdrawals) on the high street pays a paltry 1.2%.

That’s a full 2.3% below the latest inflation rate (3.5%), meaning your savings are effectively shrinking in real terms.

On a £5,000 deposit, this would add up to just £60 in interest annually, whereas the top rate currently available elsewhere could yield an impressive £239 a year.

If you’re saving for a house or a holiday that could make a REAL difference.

The truth is, you don’t need to keep your savings with your current account provider.

Most recommended savings accounts listed by comparison websites only include those covered by the Financial Services Compensation Scheme (FSCS).

This means that if the company were to go bust, your savings, up to a value of £85,000, would be protected.

So, with potential savings rates of up to 4.77% available elsewhere, why stick with your high street bank?

To find the best savings rates, use comparison websites like moneyfactscompare.co.uk and moneysupermarket.com instead of checking individual bank sites.

Look for accounts paying more interest than the current inflation rate of 3.5%.

Keep some money in an easy-access savings account for emergencies, but for long-term goals, consider fixed-rate bonds or a Stocks and Shares ISA for potentially higher returns.

Break the cycle of financial laziness

WHAT can you do about it?

- Make a list: Start by listing all your financial products including insurance policies, mortgages, savings accounts and investments.

- Set a date: Dedicate a specific time each month (or quarter) to review these. Put it in your diary.

- Comparison websites are your friend: Use comparison websites to get quotes for insurance, savings, and mortgages. They do the hard work for you.

- Don’t be afraid to switch: Once you’ve found a better deal, don’t be afraid to switch. Yes, there might be a bit of paperwork, but the savings will be worth it.

I’ve been lazy too – my biggest mistake

I learnt this hard way. Like many others, I made the classic mistake of sticking with my high street bank when I opened my first Stocks and Shares ISA years ago.

I wrongly assumed it was the best option, but my bank was quietly taking a hefty 0.25% of my entire investment’s value in fees every single quarter.

For example, if I had £10,000 saved, they’d take £25 in the first quarter alone, followed by further chunks, including a cut of any interest I earned in the following three.

And that doesn’t even include the fees to buy, sell, and trade funds and shares.

However, like me, you can get rid of these fees completely.

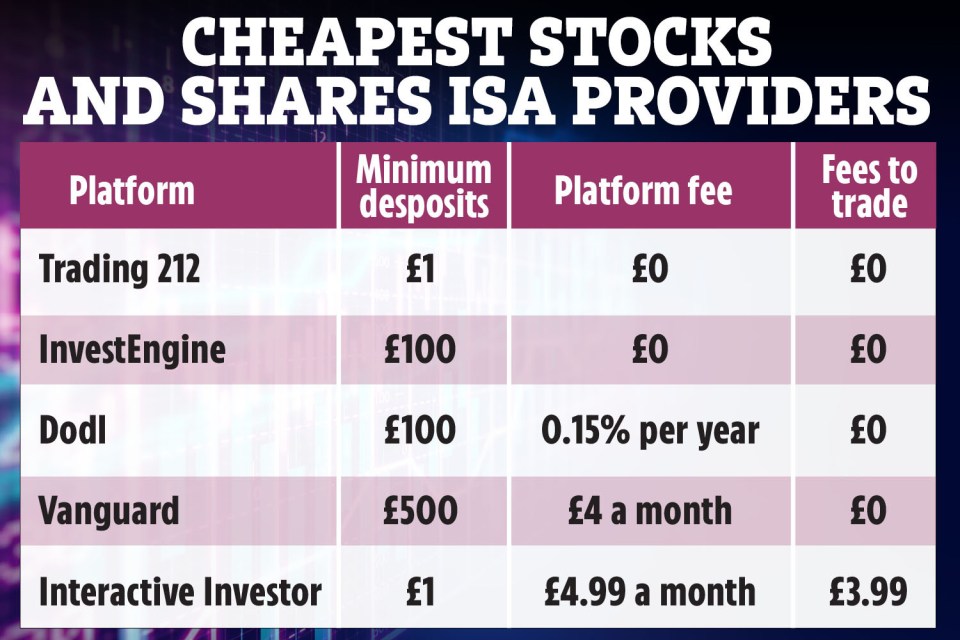

Specialist investment platforms like Trading 212 and InvestEngine don’t charge any annual fees or trading charges.

If you’d prefer to trade on a more established platform, Interactive Investor charges just £4.99 a month, and Vanguard charges £4 a month on balances below £50,000.

Of course, the exact amount you’ll be charged depends on how much you’ve invested, so grab a pen and paper and compare the fees before you get started.

Before you start investing, you need to make sure you have at least two months’ worth of salary saved into an easy access account in case of emergencies.

Most experts advise having a cash buffer to fall back on.

If you do invest – you have to be willing to lose the cash, as it’s a gamble.

But the biggest gamble of all if letting your bank or current provider scam you into taking out a product with them.

It’s rarely going to save or make you more money – but it can be avoided. It’s time to stop being lazy!

4