Planning consent for home improvement and extensions have fallen to their lowest level in a decade, according to esate agents Savills.

It revealed the number of planning consents for householder developments in England totalled 151,177 in the 12 months to March 2025.

This is 27 per cent below the preceding 10-year average, and 8 per cent down on the year, based on figures from the Ministry of Housing, Communities and Local Government (MHCLG).

The drop in planning applications comes despite house sales increasing by 24 per cent over the same period, according to HMRC figures.

Historically, there tends to be one approval for every five residential housing transactions, but this fell to one approval for every 6.8 transactions in 2024.

Decade low: Planning consents for householder developments in England totalled 151,177 during the 12 months to March 2025, which is 27% below the 10-year average

‘Typically, there is a strong correlation between property transactions and home improvements, as homeowners often undertake renovations shortly after moving in,’ said Lucian Cook, head of residential research at Savills.

‘However, this relationship became notably disjointed in 2023, with the gap between transactions and improvements reaching its widest point over the past 12 months.

‘With more properties available on the market and slightly weaker demand, our agents are reporting that buyers, who have greater choice, are increasingly favouring turn-key or ready-to-move homes.

‘Additionally, with ongoing uncertainty around the UK’s economic outlook, sentiment remains cautious.

‘As a result, many buyers are adopting a lower-risk approach and are less willing to take on the financial and logistical challenges of renovation or construction work.’

Big declines in planning consent across Britain

Home extensions and renovations continues to be most popular among buyers in London and the South, but these locations have also experienced a significant drop off in permissions.

In the 12 months to March 2025, there were 32,416 planning permissions or renovations in the South East, down by 9.3 per cent on the previous year.

However, over the past year, some of the most considerable drops have come in the North of England.

In the North East there were 4,035 planning permissions granted down from 10.7 per cent a year earlier while in the North West, there were 14,330 planning permissions granted, down 10.6 per cent on the previous year.

However, it is when looking back five years, to the 12 months to March 2020, the year before the pandemic restrictions were introduced – that we see the sheer extent of the drop off.

Compared to five years ago, The North East saw a 29 per cent drop in planning consents over the past year (the 12 months to March 2025).

The East and West Midlands also saw a 25.5 per cent drop in planning consents, while the South West saw a 23.3 per cent decline in successful planning consents.

‘The higher the house prices in an area, the more extending makes financial sense, meaning that more value can also be unlocked in London and the South compared with the Midlands and the North as build costs are less likely to outstrip the value added,’ said Cook.

‘But even in these areas the viability of construction is reacting to shifting market dynamics, with higher interest rates and weaker sentiment.

‘Rising material costs have further impacted the potential uplift across these properties, squeezing margins even in higher-value areas.’

Sky-high cost of building work to blame

The slowdown in planning applications is thought to be largely down to the increase in construction costs.

Since the end of 2019, the average cost of construction materials has climbed by more than one third, according to government ONS data.

Insulating materials and pre-cast concrete products have seen the largest increase in cost during this time, going up by more than 60 per cent.

Plastic pipes and fittings, metal doors and windows as well as cement and concrete used for bricks, tiles and flagstones have all increased in cost by more than 50 per cent during that time.

But it’s not just materials that are costing more, recent figures from Hudson Contracts show that all 12 key trades saw the average pay per week increase last year.

Electricians saw the biggest jump in pay in the 12 months to April this year, up 14.4 per cent while scaffolders saw their pay rise by 9.3 per cent on average.

‘Since Covid, construction costs have skyrocketed – with some estimates showing the price of materials for new housing has risen by 37 per cent since January 2020,’ said Steven Mulholland, chief executive of the Construction Plant-hire Association (CPA).

‘That’s been driven by everything from global supply chain disruption to soaring equipment costs, workforce shortages and rising energy prices.

‘This isn’t just a temporary squeeze – it’s a structural problem that risks making renovation and home improvements unaffordable.

‘For family-run building firms already hit by National Insurance hikes and looming changes to Business Property Relief, rising input costs are pushing business viability to the brink.

‘If we want to get Britain building again, we need a serious strategy to bring construction inflation under control and support the SMEs that power the sector.’

Lucian Cook, head of residential research at Savills

Property flipping hits lowest level since 2013

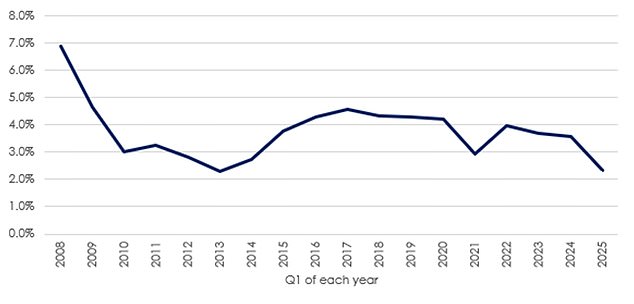

In the first three months of 2025, the proportion of homes bought and then re-sold within a year fell to just 2.3 per cent across England and Wales, according to separate analysis by property firm Hamptons.

This is down from 3.6 per cent in the first three months of 2024.

In number terms, there were 7,301 flipped homes sold in the first three months of this year, 27 per cent below the 10-year.

For someone considering flipping a home today, stamp duty (SDLT) will now account for 30 per cent of gross profit (£11,920 on average), up from 10 per cent a decade ago, before any money has been spent on improvement works.

While 80 per cent of flipped homes were sold for a higher price in Q1 2025, only 66 per cent made a profit after stamp duty costs were added.

Flipping out: In number terms, there were 7,301 flipped homes sold between January and March this year, 27 per cent below the 10-year average

Aneisha Beveridge, head of research at Hamptons, says that bigger stamp duty bills are wiping out a lot of profit from flipping.

‘The 5 per cent surcharge for investors, coupled with a reduction in the point at which buyers start paying stamp duty, means it’s harder than ever to make the sums stack up.

‘Stamp duty bills now account for nearly a third of gross profits. And in some cases, these bills are now higher than the cost of renovating the property.

‘This, together with rising material and labour costs and, in some places, falling house prices, makes flipping homes an increasingly tricky business.’