Ruined careers, decimated retirement prospects, impoverishment and even social unrest.

Those were the apocalyptic warnings made last week by the Daily Mail’s esteemed City Editor Alex Brummer.

He warned that in his 50 years writing about the economy, he had never felt so worried that a terrible financial crash was coming.

And Brummer is not alone among renowned City experts in fearing a bubble may be building up in the world’s overheating stock markets.

The signs, he said, were starting to appear all over the place.

He gave the example of tech giant Nvidia investing £100billion in OpenAI – the maker of popular AI tool ChatGPT – in a deal that is worth more than the entire value of Marmite-maker Unilever, one of Britain’s biggest companies.

Meanwhile, all the world’s major share indices, from the Dow Jones and S&P500 in the US to the Nikkei in Japan and the FTSE 100 in the UK, are at or close to all-time peaks. The same is true for gold and cryptocurrency Bitcoin.

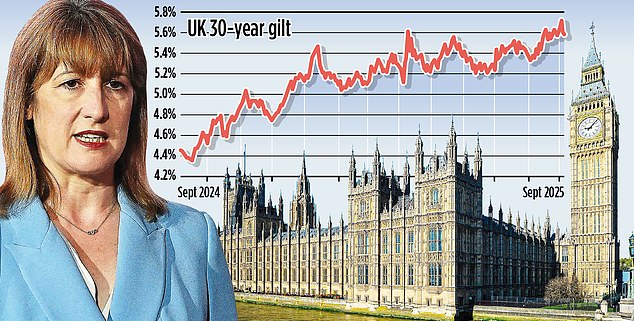

The UK’s long-term borrowing costs have soared as investors worry over the size of our debts and Chancellor Rachel Reeves’ ability to rein in spending

Government debt is also at record highs – worth almost 100pc of GDP in the UK and 140pc in the US. In Britain, in particular, high inflation is an issue, unemployment is rising and interest rates remain stubbornly high.

The big fear with markets now is if investors get jittery about a crash and start offloading their shareholdings, the panic-selling could be exacerbated in an unprecedented way by AI and computer algorithms that act automatically.

Brummer warned of an ‘unstoppable tsunami’ being unleashed – hence his warnings of potential collateral damage to the wider economy – and said the world economy and markets were now ‘teetering on a precipice’.

Scary stuff, indeed. So, if the Daily Mail’s legendary City Editor and other business experts are right to be concerned, what can you do now to protect your finances?

The answer, surprisingly, is a quite a lot. Here, we explain how to batten down the hatches and get your finances in shape for whatever comes next – whether it’s financial Armageddon, sunlit uplands or anything in between…

Jason Hollands, managing director at wealth manager Evelyn Partners, says it is understandable people are fearful, but they must avoid making rash decisions.

He says: ‘Ballooning debt-to-GDP levels across much of the globe are a concern, which have been exacerbated by the huge expansion in the size of the State during the Covid pandemic, and there are certainly some economic headwinds. ‘But, while there are some reasons to be cautious, selling up all your investments and digging an underground bunker seems excessive at the moment.’

Although it may not be time to hunker down, this doesn’t mean you should rest on your laurels. There is no way of knowing what will happen next and checking your finances are robust and can survive a storm is always a good plan.

Here is what to do now so you are protected if the worst should happen or set fair to profit if things improve.

Budgeting and debt

Getting on top of your budget and debts is the first step to sorting your finances.

In uncertain times, it makes sense to take stock and ensure you are living within your means. Make a list of incomings and outgoings and consider if there are areas where cutbacks can be made. Split spending into categories: essentials, regular needs, and discretionary and see where you can save in each one.

Read our budgeting tips and use our tool to help you.

Sorting expensive debts should be a priority. Look at the interest rate on any loans or credit cards and see if you can get a better deal. If possible, shift credit card debt to a 0pc balance transfer card. These charge no interest for a set period, so are a good way of clearing a balance faster.

Sarah Coles, of investment platform Hargreaves Lansdown, says: ‘Steer clear of overstretching and aim to have enough room in your financial life to cope with the unexpected.’

Once you have a handle on your budget and any debts, you can work out how much you can afford to save and invest each month.

Savings

Having a buffer in case of an unexpected expense is always important, but it’s wise to build this further in turbulent times. As a general rule of thumb, aim to have three to six months of essential spending in cash in case of an emergency.

Keep emergency cash in an easy-access account, where you can get to it with no notice or penalty. Look for market-leading deals to ensure you are still earning interest on this pot. Check our independent best buy savings tables compiled by Sylvia Morris.

An instant access flexible cash Isa lets you take money out if you need it and you won’t pay tax on interest. Trading 212’s cash Isa pays 4.38pc, while Ford Money’s pays 4.18pc, and neither limit withdrawals.

Outside of an Isa, Chase Bank currently pays up to 4.5pc on its easy-access account. Spring, part of Paragon Bank, offers 4.3pc with interest paid monthly.

Fixed rate savings can lock in higher rates for longer but won’t allow access to your funds.

Consider a ‘staircasing’ approach to savings, where some is kept in easy-access, another chunk in a one-year fixed rate bond, a further chunk in a two-year bond, and so on. This allows you to secure a decent rate of interest for the long term, without locking up all your money.

Dan Coatsworth, of investment platform AJ Bell, says: ‘Those worried about a dip in the economy might want to squirrel away a bit extra and cut back on a few luxuries. It’s better to make a few sacrifices with spending and be able to sleep soundly at night than keep splashing the cash and regret it later.’

Mortgages

Mortgage rates are priced off money market funding costs, which are influenced by expectations for the Bank of England’s base rate.

How far or fast interest rates will fall is unclear, as the Bank’s rate setters are in a bind due to low economic growth combined with high inflation at 3.8pc. Typically, when growth is low, the Bank cuts interest rates to encourage borrowing, spending and to boost the economy.

However, when inflation escalates, rates tend to stay higher to slow things down and tackle rising prices.

Banking industry group UK Finance estimates about 1.8 million fixed rate mortgage deals are ending this year and another 1.9 million in 2026. These borrowers have been desperately hoping for cuts, but the decline in mortgage rates has stalled with the best two and five-year fixes stuck at just below 4pc.

It is possible to secure a mortgage rate up to six months before your current deal ends, and you can move to another if a better rate emerges before the new deal takes effect. Speak to an independent broker well ahead of time to discuss your options.

If you believe interest rates have further to fall, you might have to consider a tracker or variable rate. This is a risk as it could mean higher repayments in the short-term – and there is no guarantee rates will drop.

Make sure you do not end up on the lender’s standard variable rate (SVR) – this is the rate you are automatically moved to when a deal ends and is significantly more expensive. Britain’s biggest mortgage lender, Halifax, currently has an SVR of 7.24pc.

Anyone still locked into a deal can consider making overpayments. This should mean they can either reduce the term of their loan or get access to a better deal next time they come to fix, by reducing their loan-to-value ratio. Check how much your mortgage allows you to overpay and watch out for early repayment charges.

You can compare the best mortgage deals you could apply for with our mortgage finder tool.

Pensions

Those closer to retirement should consider when they plan to access their savings, how much money they will need to live on, and how best to tap into their pot.

Those with defined benefit pension schemes, commonly known as final salary pensions, will have a guaranteed income paid by their former employer.

Savers with defined contribution schemes will have built up an investment pot that they must turn into retirement income.

The two main options are to leave your pension invested and draw on it for income or to use the pot to buy an annuity, which pays a guaranteed income for life. You can mix and match these.

A sharp fall in your pension pot’s value just ahead of retirement due to stock markets tumbling can be extremely worrying.

If you plan to stay invested for the long-term and draw on the pot, then you have time to ride out the storm but advisers recommend dialling back withdrawals when markets are down.

If you want to buy an annuity, then protecting your pot’s value close to retirement is critical.

You could consider moving a portion of your pension investments into less risky assets, which may not be as volatile in a market fall.

‘[In the event of a crash] you might have to choose between retiring with a lower income than you originally hoped for or continue working until your savings recover,’ warns Craig Rickman, personal finance editor at Interactive Investor.

Entirely cashing in your pension is unlikely to be a good idea. Not only does this take your cash out of a very tax-efficient environment, but it also means you lock in any losses – and could land you with a very large tax bill to boot.

Younger savers can benefit from falling markets as their monthly contributions will buy more shares, boosting their pot when markets recover.

If you’re decades from retirement the advice is to stay calm and save. ‘Keep paying into your pension and don’t be tempted to reduce your investment risk,’ says Mr Rickman.

Nvidia’s huge deal with Open AI has raised fresh fears of a stock market bubble

Investments

When it comes to investing, timing the perfect moment to buy and sell is nigh-on impossible. Selling out during a downturn can mean you miss significant gains when the market recovers. However uncomfortable it feels, staying invested is usually the best strategy, as long as you don’t need to access your cash in the near future.

Mr Hollands says: ‘If you are going to need your money within 12 months, you shouldn’t be invested in the stock market as it is too volatile. If you have decades to invest, then don’t be distracted by near-term worries about economic uncertainties.’

A good tidy-up of your portfolio is always sensible, however. Review your portfolio and ensure it is well diversified. Mr Coatsworth says: ‘That means having exposure to different assets like shares, bonds, commodities such as gold and property, as well as to a range of sectors and geographies.’

Consider your risk appetite and whether your portfolio is aligned with this. Many global stock markets have been on a stellar run this year so you may need to rebalance. This means taking some profits from your top performers and reinvesting the proceeds into other funds or markets.

Gold and bitcoin

Gold is traditionally viewed as a safe haven in times of turmoil, and its price has soared to record highs this year. The precious metal could rise further as central banks across the world, and particularly in emerging markets including China, continue to buy in bulk.

Interest in gold could be further bolstered as the US dollar – another traditional safe haven – weakens, causing investors to look elsewhere for surety, says Kate Marshall, senior investment analyst, Hargreaves Lansdown.

Having a small proportion of your portfolio invested in gold can provide some ballast against a downturn.

The easiest way to do this is by investing in a low-cost exchange-traded commodity (ETC). This is a stock market listed fund that tracks the price of gold – such as the iShares Physical Gold ETC, which charges just 0.12pc and has returned 41.3pc over one year.

Another option is to buy physical gold bars, but bear in mind the cost of storing it securely and that it can take longer to sell, if you need the money.

‘Gold should be seen as one part of a diversified portfolio rather than a standalone solution,’ adds Ms Marshall.

Cryptocurrency bitcoin has been touted as ‘digital gold’ but, as a relatively new asset its performance as a store of value is untested compared to gold’s record that runs into centuries.

Bitcoin is also hugely volatile and so should be considered a high risk rather than defensive investment when global markets look uncertain. ‘As a speculative asset, no one really knows if bitcoin will rise or fall. As such, the potential for consumers getting their fingers burnt is great,’ says Ian Futcher, financial planner at Quilter.

Those who like the idea of owning some cryptocurrency as a means of diversification should be sure to use a trusted platform, regulated by the FCA, and only invest a small proportion of their total assets.

Labour’s national insurance hike for employers has been blamed for sending the jobs market into reverse – meaning it’s a good time to protect yourself

Jobs

While economic growth is likely to remain sluggish, the UK is not in recession territory – yet. However, increases to the National Insurance tax paid by employers raised costs for businesses, some have made redundancies, and the jobs market has cooled dramatically.

Business leaders including Next chief executive, Lord Wolfson, retail veteran, Lord Rose, and Wetherspoons founder Sir Tim Martin, have all sounded the alarm over the jobs market.

Meanwhile, electricals retailer AO World’s boss John Roberts last week said he feared we were heading into a recession. Now could be a good time to consider whether there is anything you could do to bolster your job prospects.

Ms Coles says: ‘This might mean polishing up your CV, increasing your networking, and working on new skills or experiences that could put you in a better position both in your current role and the wider jobs market.’

Employed workers should check their contract to understand their notice period and what they may be entitled to in the event of redundancy or if they cannot work due to ill health.

Income protection insurance won’t usually cover redundancy but will pay a monthly amount if you become ill or get injured and cannot work. Employees and particularly the self-employed should consider this.

If you are self-employed, also make sure you have enough money set aside to cover your tax bill, and keep it in a separate account so you are not tempted to spend it.

What else?

When people become fearful about the economy, it can lead to irrational behaviour.

Rather than getting swept up worrying about the ‘what ifs’, focus on the potential risks facing you personally – and consider the steps you can take to mitigate them, says Ms Coles.

Is your fixed rate mortgage up for renewal, do you worry when your investments fall in value, is your job in a tricky part of the economy, do you only have a small rainy-day fund, are you self-employed and your family relies on your income?

If the answer to some of the questions above is ‘yes’, then it is probably time to make your finances more resilient.

In contrast, if you are mortgage-free, have a reliable job with a long notice period, plenty of savings and investments, or a good final-salary pension, then you may be able to relax and even spend a bit more to help the economy.

Whatever your financial situation, make the most of your money and save where you can.

Use this time to review household bills. Could you save money by switching to a new insurance provider or energy deal, for example? Go through recent bank statements to see if you are paying for things you no longer use, have a forgotten gym membership, or just having too many takeaways.

Richard Cook, senior financial planner at wealth manager Rathbones, says: ‘A crash is a stress test for your finances. Preparation turns uncertainty into reassurance and keeps you calm when markets are anything but.’

SAVE MONEY, MAKE MONEY

Sipp cashback

Sipp cashback

£200 when you deposit or transfer £15,000

4.51% cash Isa

4.51% cash Isa

Trading 212: 0.66% fixed 12-month bonus

£20 off motoring

£20 off motoring

This is Money Motoring Club voucher

Up to £100 free share

Up to £100 free share

Get a free share worth £10 to £100

No fees on 30 funds

No fees on 30 funds

Potentially zero-fee investing in an Isa or Sipp

Affiliate links: If you take out a product This is Money may earn a commission. These deals are chosen by our editorial team, as we think they are worth highlighting. This does not affect our editorial independence. Terms and conditions apply on all offers.