The state pension age should be hiked by a year once a decade to make it more affordable, but everyone would get at least a five-year payout under a new plan floated by pension experts.

A series of increases, giving people fair advance notice, would address massive improvements in life expectancy that have stretched time spent in retirement, according to former Pensions Minister Steve Webb and longevity expert Stuart McDonald.

The qualifying age is currently 66 and is already set to rise to 67 between 2026 and 2028, but a new Government review has triggered speculation it might have to rise substantially to contain rapidly rising costs.

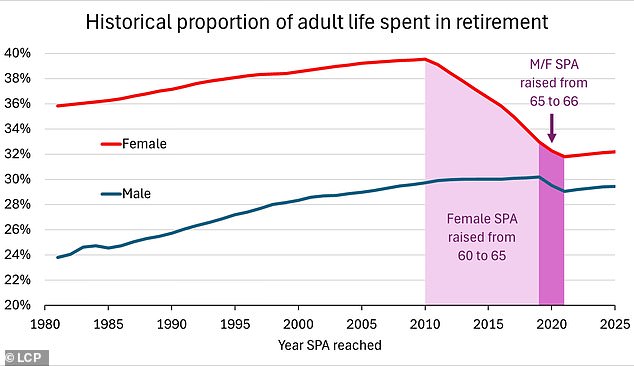

During the last century the life expectancy of young adults rose by 17 years, say Webb and McDonald. Yet state pension ages remained at 65 for men and 60 for women, until from 2010 women’s age was raised so they were equal at 65 and then both were raised in tandem to 66.

Baby boys born now can expect to live until age 87 and girls until 90, according to the Office for National Statistics average life expectancy calculator here.

However, not all newborns will live to state pension age. If you have already survived to 66, life expectancy for men that age is currently 85 while for women it is 88.

A possible timetable for 10-yearly increases is set out below – but the plan would also introduce a new ‘guarantee’ so people whose lives are cut short and their families don’t lose out entirely.

Current timetable for state pension age rises compared with plan from LCP

How would radical idea to hike state pension age work?

Under what is dubbed a ‘something for something’ reform, the imbalance caused by life expectancy would be addressed, but everyone who reached state pension age would be guaranteed at least five years of payments

This money would go to beneficiaries if someone didn’t live long enough to receive it themselves.

Meanwhile, similar arrangements could be made for people who die before state pension age, based on their record of National Insurance contributions to date.

The guarantee would help ‘square the circle’ between the need to increase the state pension age and the need to avoid penalising those whose life expectancy is lower than average, according to Webb and McDonald, both partners at pension consultant LCP.

They also suggest changing the expectation that people will spend a up to a third of their adult life in retirement, because ‘locking in’ at this historically unprecedented level is unsustainable.

They argue that setting state pension age so that people can on average expect to receive a state pension for a fixed period such as 20 years would put funding the system onto a firmer level.

That would mean retirements would stay the same length but working lives would lengthen, making the system more affordable, they say.

People are spending longer periods of their lives in retirement due to massive improvements in life expectancy

Webb, who is also This is Money’s retirement columnist, says: ‘The case for increasing state pension ages is strong, but it has always been hard to do so in a way that is fair to people in more deprived areas who cannot expect to draw a pension for as long.

‘Those who have paid in to the system all of their lives would be guaranteed that they or their heirs would get a minimum payout once they start drawing a pension. This would be a concrete way of addressing concerns over unfairness each time state pension ages are increased.’

McDonald says: ‘We now have historically long retirements which will inevitably prove fiscally unsustainable. A new approach is needed. We recommend setting pension ages on the basis that the average person can expect a fixed number of years in retirement.

‘This will help the system to catch up with the dramatic improvements in life expectancies which we have seen, and will be fairer to current and future people of working age, whose contributions are used to pay the pensions of retirees.’

What about the triple lock?

The Government has effectively, if not in so many words, told the experts officially reviewing the state pension age to operate on the assumption that the triple lock pledge will remain in place indefinitely.

This means the state pension should increase every year by the highest of inflation, average earnings growth or 2.5 per cent.

The Government has promised to stick to the triple lock for the whole of this parliament. The pledge is popular, but critics point out that maintaining it is expensive when public finances are in a straitened state.

The Institute for Fiscal Studies has said retaining the triple lock while raising the state pension age would hit poorer people more.

It says this is because the loss of a year of state pension income is more important for those with lower life expectancy which poorer people tend to have, while those with a higher life expectancy benefit relatively more as they might receive a generously indexed state pension into their 90s and beyond.

Webb and McDonald note in their report: ‘We have had decades of rising inequalities with most increases in life expectancy accruing to those who already lived longer, while poorer groups have seen less improvement.

‘For example, the most deprived 10 per cent of women saw their life expectancy fall between 2011-13 and 2017-19 while less deprived women, and men, saw life expectancy gains of around six months over the same period.

‘Under the current formulaic approach, it would be theoretically possible, if inequalities continue to widen, for state pension age to be driven ever higher by the experience of long-lived affluent groups, growing ever more out of reach to deprived groups who die before state pension age.’

When can you retire? State pension age is set to rise to 67 between 2026 and 2028

When will the state pension age rise again?

The rise to 67 is already set to happen between 2026 and 2028, but the next increase to 68 is still up in the air.

The Government is expected to give at least 10 years’ notice of a change in the timetable, but it could act straight after the current official review concludes in 2029.

This could mean the rise to 68 is accelerated to 2039-41, which would affect workers now aged 51, 52 and 53.

The full state pension is currently worth £230.25 a week or nearly £12,000 a year if you have paid enough National Insurance years to receive the full amount. It is due to rise by 4.8 per cent to around £241.40 a week a week or £12,500 a year from next April 2026.

Meanwhile, the minimum pension age for accessing workplace and other private retirement savings is due to rise from 55 to 57 from April 2028.

Governments have in the past tended to keep the state pension and private pension ages roughly 10 years apart, so any future increases could well continue to happen in tandem.

SIPPS: INVEST TO BUILD YOUR PENSION

AJ Bell

AJ Bell

0.25% account fee. Full range of investments

Hargreaves Lansdown

Hargreaves Lansdown

Free fund dealing, 40% off account fees

Interactive Investor

Interactive Investor

From £5.99 per month, £100 of free trades

InvestEngine

InvestEngine

Fee-free ETF investing, £100 welcome bonus

Prosper

Prosper

No account fee and 30 ETF fees refunded

Affiliate links: If you take out a product This is Money may earn a commission. These deals are chosen by our editorial team, as we think they are worth highlighting. This does not affect our editorial independence.