Landlords have been delivered a hammer blow by the Chancellor in today’s Budget.

Rachel Reeves announced that the tax property investors pay on their rental income will be levied at higher rates from April 2027.

The change will see landlords taxed at 2 percentage points above normal income tax rates. Basic rate tax paying landlords will see their rental income taxed at 22 per cent, up from 20 per cent.

Meanwhile, higher rate tax-paying landlords will see their rental income taxed at 42 per cent, up from 40 per cent today, while additional-rate taxpayers will be taxed at 47 per cent, up from 45 per cent currently.

The Office for Budget Responsibility (OBR) says this is estimated to bring in £500million a year for the Treasury per year from 2028-29.

Buy-to-let blow: Income tax charged on rental income for landlords will rise by 2 percentage points across the board from 2027

The changes will reduce returns for landlords who have already been pounded by higher taxes and increased regulation since 2016.

In her previous Budget in October 2024, Rachel Reeves added a 2 per cent stamp duty surcharge on top of the extra 3 per cent landlords already pay, adding thousands of pounds to the cost of buy-to-let and second home purchases.

Landlords who own property in their own name, rather than in a company structure, are also now unable to fully offset mortgage interest costs against their tax bill as they did previously.

Jason Tebb, president of property portal OnTheMarket, thinks the additional tax on rental income is ‘disastrous’ for landlords.

‘This reform will simply see more and more landlords removing themselves from the private rental sector for a further squeeze on rental supply,’ he said.

How much more tax will landlords pay?

Landlords who own buy-to-lets in their own names, rather than through a limited company currently pay income tax on their rental profit.

What a landlord receives in rent is added to whatever other income they earn to establish what rate of tax they pay.

A landlord with annual income between £12,571 and £50,270, including their earnings from rent and their salary, therefore pays 20 per cent tax.

Above that, they pay 40 per cent tax on the portion of their earnings between £50,271 and £125,271 and 45 per cent tax on anything above that.

This means a basic rate taxpayer earning £10,000 of rental profit pays £2,000 in income tax on the rental profit, while a higher rate taxpaying landlord earning £10,000 of rental profit pays £4,000 in income tax on the rental profit.

The rental profit is the amount left over after other costs have been deducted, such as letting agent fees and repairs.

The Chancellor’s announcement today will mean a basic rate tax paying landlord with £10,000 rental profit will go from paying £2,000 to £2,200 in tax, while a higher rate tax paying landlord will see their tax bill rise from £4,000 to £4,200.

Landlords who have a mortgage on their property will feel the pinch more acutely, as their outgoings are higher. This applies to some 2 million landlords, according to UK Finance figures.

| Rental income (after expenses) | £12,000.00 | £18,000.00 | £24,000.00 | £30,000.00 |

|---|---|---|---|---|

| Extra tax for basic rate taxpayer | £240.00 | £360.00 | £480.00 | £600.00 |

| Extra tax for higher rate taxpayer | £240.00 | £360.00 | £480.00 | £600.00 |

| Extra tax for additional rate taxpayer | £240.00 | £360.00 | £480.00 | £600.00 |

| Source: Hargreaves Lansdown |

New tax could mean rents will go up

Property industry experts say the new tax could be the final straw for many landlords who are already coping with increasing legislation, including the Renters Rights Act, which comes into force on 1 May next year.

The OBR says successive tax hikes on private landlord returns will reduce the supply of homes to rent over the longer run and says ‘this risks a steady long-term rise in rents’ if demand for properties outstrips supply.

Colleen Babcock, a property expert at Rightmove thinks landlords will increase their rents to cover the extra 2 percentage points of income tax.

‘Landlords might look like an easy target, but rental market taxation is usually detrimental to tenants looking to rent a home,’ says Babcock.

‘The simple fact is that in order to provide tenants with much-needed homes, investors need to be able to make the sums add up.’

Julian Bradshaw, director at the chartered financial advisers Smith & Pinching thinks the 2 per cent increase in property income tax will leave thousands of landlords struggling to make the sums add up.

‘Unless they’re able to remortgage onto a dramatically cheaper mortgage, many will see their profits disappear completely,’ says Bradshaw.

‘Capital appreciation has weakened too, as official data shows property prices are rising only slowly or even falling in some parts of the country.

‘As a result, many amateur or ‘accidental’ landlords may conclude that the hassle of property ownership is no longer worth the meagre income it generates.’

Major tax shake-up: Higher rate tax-paying landlords will see their rental income taxed at 42% from 2027, up from 40% today

More landlords will buy in companies

Landlords buying properties have two options – to do so in their own name, or to set up a limited company and buy the property within that. Properties can be switched from one to the other.

Given the tax changes of recent years, many landlords see buying within a limited company as a way to pay less tax.

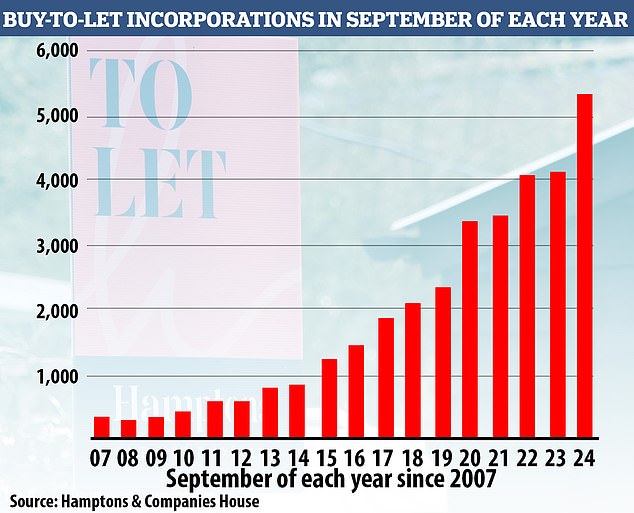

The companies have surged in recent years and a record 70,000 companies are likely to be set up by the end of 2025, according to Hamptons.

Mark Harris, chief executive of mortgage broker SPF Private Clients, said: ‘This Budget is the final nail in the coffin for landlords owning property in their own name.

‘It is very hard to make a profit unless property is owned via a limited company structure.

‘We have seen a growing number of clients either purchase investment property via this route or move existing portfolios in their own name over to a limited company structure and we now expect this trend to escalate.’

Owning in a limited company allows property investors to fully offset all of their mortgage interest against their rental income, before paying tax.

Tax perks: As the gap between personal and corporate tax rates widen further thanks to the Budget, there is likely to be more landlords incorporating

This differs from landlords who own property in their own name. They only receive tax relief based on 20 per cent of their mortgage interest payments.

This is less generous for higher-rate taxpayers, who previously received 40 per cent tax relief on mortgage costs before a 2016 rule change.

A higher-rate taxpayer landlord with mortgage interest payments of £500 a month on a property rented out for £1,000 a month now pays tax on the full £1,000, with a 20 per cent rate on the £500 that is being used towards the mortgage.

A landlord who owns in a limited company with mortgage interest payments of £500 a month on a property rented out for £1,000 a month would only pay tax on £500 of that income.

Put simply, it means that whilst individual landlords are effectively taxed on turnover, and company landlords are taxed purely on profit.

There are also other advantages of buying property via a limited company, including the fact that corporation tax – payable in a company structure – is lower than income tax, which is payable for landlords who own properties in their own name.

This allows landlords to build up profit within the company, which they can use it to re-invest towards another property sooner than they might otherwise have done if owning in their own name.