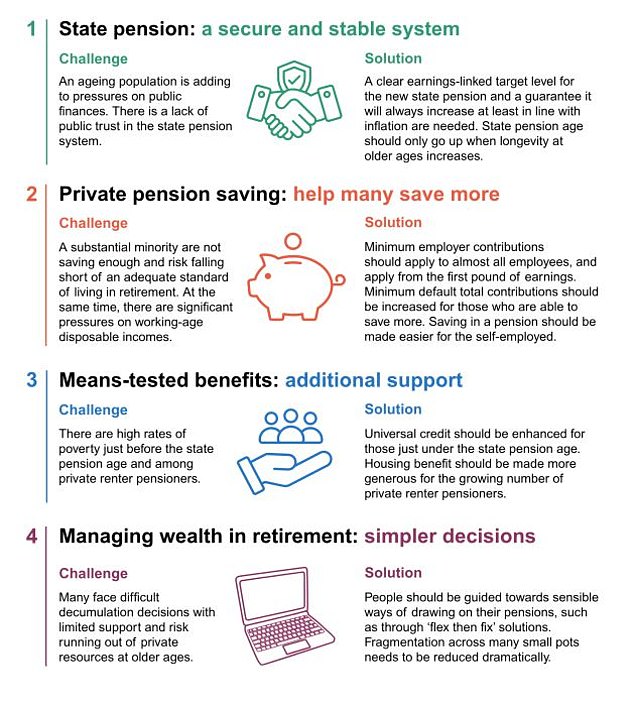

The Government is being urged to commit to never means-test the state pension in an overhaul floated by think-tank the Institute for Fiscal Studies.

But it says the popular triple lock should be ditched in the longer run, in favour of keeping the state pension in line with earnings growth or inflation every year.

The state pension is worth £230.25 a week or nearly £12,000 a year if you’ve paid enough in to get the current full rate – and it’s the bedrock of most people’s retirement income.

Under the triple lock the state pension is increased every year by the highest of inflation, average earnings growth or 2.5 per cent.

The IFS is recommending sweeping changes to private and state pensions to create a system ‘fit for the next generation’, ahead of a pending Government review of pension adequacy.

Decisive action is needed – including new rules for raising the state pension age – it says in a new report published in partnership with Abrdn Financial Fairness Trust.

The future of pensions: Less secure incomes and lower home ownership among older people lie ahead

What are the proposals to overhaul pensions

Pensions have undergone major improvements in recent decades, but serious problems remain for the next generation of pensioners, according to the IFS.

It is pushing the following reforms.

– The Government should choose a target level for the state pension, set as a percentage of average earnings in the wider economy, and keep using the triple lock to decide annual increases until it is reached.

After that it would be hiked in line with average earnings growth, or inflation if that is higher.

Currently the state pension is worth 30 per cent of median – meaning the middle value, not average – full-time earnings.

– The state pension age is currently 66, and between 2026 and 2028 it will rise to 67 – but the next rise to 68 is still up in the air.

The IFS says it should only rise as longevity at older ages rises, but by less than that – meaning the average time spent receiving the state pension would increase.

– Auto enrolment into work pensions should be changed so employers have to put at least 3 per cent into a pension for every staff member, even if they are not making minimum contributions themselves.

Workers must currently put in 4 per cent, plus they get 1 per cent in tax relief from the Government.

– The age limits should also be widened from 22-66 to 16-74, and the band of earnings pension contributions are based on changed from £6,240-£50,270 to £4,000-£50,270, says the IFS.

– Minimum contributions should be raised but only for the better-paid.

For those earning at least £10,000 per year, the minimum default contribution would be 3 per cent of £9,000, plus 10 per cent of the portion of earnings between £9,000 and £90,000. That would mean someone on £35,000 per year paying in an extra £570 a year.

But you would be allowed to contribute less, as well as more, than these defaults if you wanted.

– The self employed should be helped to save into pensions by integrating contributions into their self-assessment tax returns.

– Universal Credit should be boosted for people within one year of their state pension age, based on either low incomes and assets or health conditions.

– Housing benefit should be increased for pensioners living in private rented accommodation, based on the local rents of at least a two-bedroom property.

– Retirement income products known as ‘flex then fix’ – drawdown in the early years followed by an annuity later – should be encouraged.

What is wrong with pensions – and how to fix them

The IFS says fewer future pensioners are going to benefit from generous ‘defined benefit’ pensions – guaranteed until you die, with no investment risk for the individual – or high levels of home ownership, or rising house prices.

People now have to make more complex decisions over how to manage and live on their pensions during retirement, it says.

It also notes that many workers are failing to save enough to have an adequate income in retirement – including the self-employed, 80 per cent of whom are not saving into a private pension.

Meanwhile, increasing numbers of older people are living in more expensive, insecure private rented accommodation.

And all this is happening while the Government is facing pressure on public finances from an ageing population.

The IFS says its proposals are aimed at:

– Providing a secure state pension;

– Increasing the number of workers saving into a private pension and helping others to save more;

– Giving increased and targeted support to those hit hardest by state pension age rises and others at risk of poverty;

– Helping people manage their pension through retirement.

David Gauke, former Tory Work and Pensions Secretary, chaired the steering group of the IFS’s Pensions Review, which has been doing research for the past two and a half years.

‘Pensions need long-term planning and, ideally, a broad consensus,’ he says. ‘The proposals put forward maintain an important balance between the state, employers and workers.

‘The Government should provide a secure pension income, further increases in the state pension age should be accompanied by more support for those hardest hit, and both employees and employers should gradually contribute more to help achieve greater financial security in retirement.’

Paul Johnson, director of the IFS, says: ‘There is much to celebrate about the current UK pensions system. The current generation of retirees is, on average, doing much better than any previous generation.

‘Pensioner poverty is way down on the very high levels in the 1970s and 1980s, and is indeed below that for other demographic groups. The state pension has been simplified and is now much more generous to many women than in the past.

‘Many more employees have been brought into workplace pensions by the successful roll-out of automatic enrolment.

‘But there is a risk that policymakers have become complacent when it comes to pensions.’

Abrdn Financial Fairness Trust, funder of the Pensions Review, says: ‘Many low earners are set to face financial difficulties when they retire, with one in three low earners currently saving into defined contribution pensions not on track to achieve a standard benchmark for an adequate retirement income.

Many are not saving at all, especially the self-employed. This poses serious problems for individuals as well as the state, and action is needed sooner rather than later to avoid problems growing and to future-proof pensions.’

IFS wants shake-up of private and state pensions

SIPPS: INVEST TO BUILD YOUR PENSION

AJ Bell

AJ Bell

0.25% account fee. Full range of investments

Hargreaves Lansdown

Hargreaves Lansdown

Free fund dealing, 40% off account fees

Interactive Investor

Interactive Investor

From £5.99 per month, £100 of free trades

InvestEngine

InvestEngine

Fee-free ETF investing, £100 welcome bonus

Prosper

Prosper

No account fee and 30 ETF fees refunded

Affiliate links: If you take out a product This is Money may earn a commission. These deals are chosen by our editorial team, as we think they are worth highlighting. This does not affect our editorial independence.