Have you saved wisely, invested well and built up a healthy pension to enjoy in retirement and pass down to your loved ones?

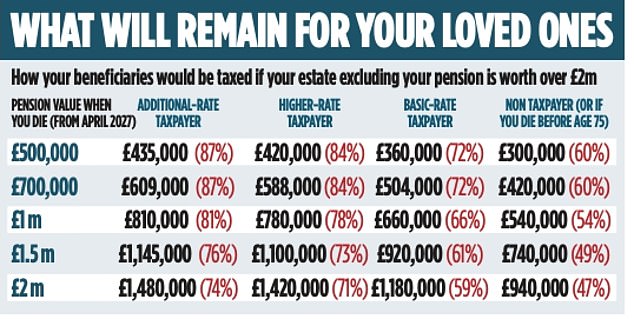

Then beware. Up to 87 per cent of it could be swallowed up in tax when you die once new inheritance tax rules are introduced in 2027, Wealth & Personal Finance can reveal in our new calculations.

Pensions are currently exempt from inheritance tax, which has made them a popular vehicle to pass on wealth to the next generation. All other assets attract inheritance tax at a flat rate of 40 per cent, once you have exceeded your allowances.

From April 2027 pensions will be considered part of your estate for inheritance tax calculations following changes announced by Chancellor Rachel Reeves in her Autumn budget last year.

But overlooked quirks in the rules mean that in some cases pensions could be taxed at a far higher rate than 40 per cent – in some cases as high as 87 per cent.

Experts explain why this can happen – and what you can do to protect yourself.

HOW DOES THE QUIRK COME ABOUT?

Everyone has two main allowances that permits them to pass on a proportion of their assets free from inheritance tax.

The first is called the nil-rate band, which allows you to hand over up to £325,000 free of inheritance tax. Couples who are married or in a civil partnership can combine their allowances to pass on up to £650,000 tax free.

The second is the residential nil-rate band, which is an extra allowance if you are passing on a family home to direct descendants such as children. In this case, you can pass on a home worth up to £500,000 free of inheritance tax – or £1 million for couples.

However, if your total assets exceed £2 million, you start to lose your residential nil-rate band. It is reduced by £1 for every £2 that your estate exceeds £2 million. That means you lose your allowance altogether if your estate is worth more than £2.35 million – or £2.7 million for couples.

NOW let’s calculate the inheritance tax bill when your pension is considered part of your estate.

If a couple had a family home worth £2 million and pension savings of £700,000, under today’s rules their total taxable estate for IHT purposes would be £2 million. This is because pensions are not yet included. They could use their residential nil-rate band to pass on the £1 million from the family home tax free. The remaining £1 million would be taxed at 40 per cent, resulting in an inheritance tax bill of £400,000.

But from April 2027, their taxable estate would be £2.7 million, because the pension would be included. Their full residence nil-rate band would be tapered away and they would only have the £650,000 nil-rate band to cut their inheritance tax bill.

Their beneficiaries would pay 40 per cent on the £2.05 million that is liable for tax, resulting in a total tax bill of £820,000 – more than double the £400,000 amount that would be charged today. Of the £2.7 million that they have to pass on, their loved ones would receive just £1.88 million.

Of the £420,000 additional tax your beneficiaries would pay from April 2027, £280,000 is IHT on the pension (40 per cent of £700,000) and the other £140,000 is from losing your residence nil-rate band (40 per cent of £350,000). But the tax doesn’t stop there, because if you die after the age of 75, your beneficiaries must pay income tax at their marginal tax rate when they make withdrawals from your pension.

For basic rate taxpayers this would be 20 per cent, but for additional rate taxpayers, this could amount to a tax of 45 per cent. In this case, the result is that once all the tax has been paid, your beneficiaries could end up with as little as 13 per cent of the pension that you left them – just £91,000 of the original £700,000.

Carl Roberts, a chartered financial planner at RTS Financial Planning, says: ‘One tax is bad enough, but to apply a second tax once the beneficiaries have the pot is just plain greedy. It’s an absolute betrayal of pensioners who have spent years saving, investing and building what is likely to be their second biggest or in some cases, biggest asset.’

‘The Government may say pensions were never meant to be a way of passing down benefits and are supposed to be for spending in one’s retirement. But if you’ve been a diligent saver your whole life, you are very unlikely to spend down your pension,’ he says.

MORE FAMILIES WILL BE HIT

The number of deaths that result in an inheritance tax bill is currently around 4.35 per cent, according to HMRC. But the number is likely to rise substantially once pension savings are included – particularly in the South East and London. The average house price is £552,000 in London and £386,000 in the South East, while the average pension pot for someone aged 65 is more than £190,000. Many families here are likely to be close to the IHT threshold.

The standard £325,000 IHT allowance has not changed since 2009, while the additional property allowance has been unchanged at £175,000. These thresholds will remain frozen until at least 2030.

Inheritance tax receipts were £8.2 billion in the year from April 2024 to March 2025 – up 11 per cent on the year before. IHT receipts were £800 million in April 2025 alone, up 14 per cent year-on-year, figures from HMRC show.

Around 4,500 households in London and 5,860 in the South East paid inheritance tax in the 2021/22 tax year, according to the latest HMRC data. This compares with 325 in Northern Ireland and 484 in the North East.

THE STEPS YOU CAN TAKE

If you have an estate worth more than £2 million, one option could be to give money away. This would allow you to keep the full residence nil-rate band of £350,000 per couple (or £175,000 per person).

Jonathan Halberda, a financial adviser at Wesleyan Financial Services, says: ‘Giving gifts of money or assets to loved ones is one of the most straightforward ways to reduce your inheritance tax.’

You can give away £3,000 each tax year without worrying about inheritance tax. Go to: gov.uk/inheritance-tax/gifts.

You can also give away larger gifts, so long as you live at least seven years after making the gift. If you die within seven years, it will reduce your main inheritance tax allowance.

Remember that the plan to include pensions for inheritance tax purposes is still in the proposal phase and nothing has been clarified yet. So, think carefully before making any rash decisions. A financial adviser or wealth planner will be able to help you work out what is right for you and your family. The rules can be complicated, so seeking expert advice would be worthwhile.