IF you’re employed and over the age of 22 – then there’s a secret way to give yourself a pay rise.

Journalist Sara Benwell, who has almost two decades of experience writing about personal finances, explains how you can do it.

2

Saving for retirement might not be top of your list when you’re young, especially in a cost of living crisis with rising energy bills, rent and weekly shopping stretching your budget.

But it is vital that you start early to allow your cash to grow and you don’t need to part with loads of cash to get started.

Thanks to auto-enrolment rules, anyone aged between 22 and state pension age, who earns more than £10,000 a year with a single company is automatically signed up to a pension.

You’ll have to pay a certain percentage of your income in, but the great news is your employer must also contribute, which means they’re adding free money to your savings. You’ll also benefit from tax relief from the government.

And that money is invested by experts on your behalf so it can get bigger over time.

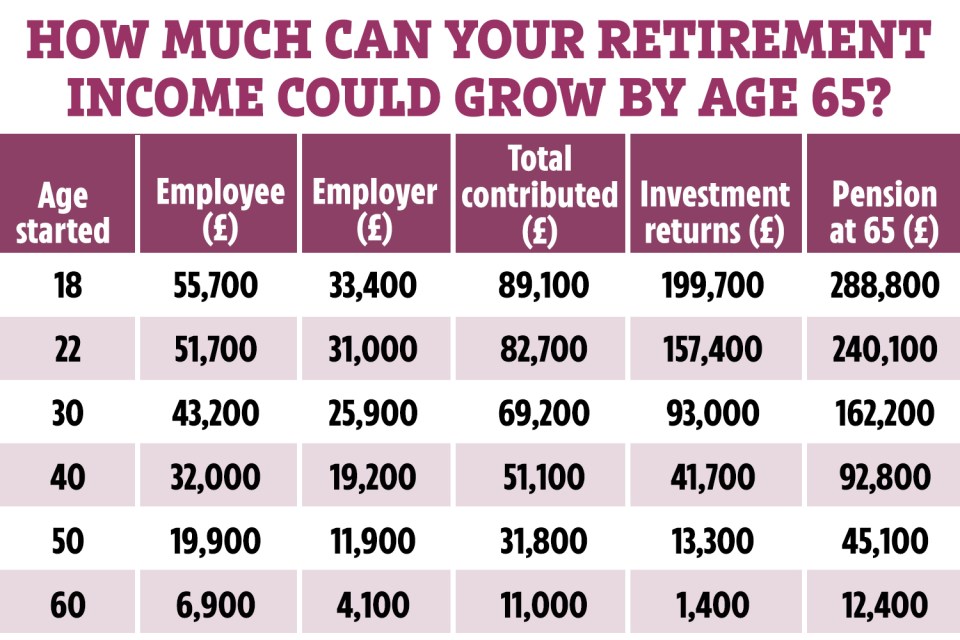

Exclusive figures provided by Aon to the Sun show that someone who starts saving at age 22 and only pays in the legal minimum could still end up with £240,100 by the time they retire.

Wait until you’re 40 and you’ll only get £92,800 – nearly £150,000 less.

So how does it work? Who’s eligible? And how can you make the most of it?

What is auto-enrolment?

Auto-enrolment is a UK law that says employers must sign most workers up to a pension scheme.

To qualify, you must be:

- Aged 22 or over

- Under State Pension Age

- Earning more than £10,000 a year

- Working in the UK

If you meet all those criteria, your employer must pay at least 3% of your salary into a pension for you.

You’ll pay in 5%, making a total minimum of 8%.

You can opt out, but that means turning down thousands of pounds in employer contributions, government top-ups, and long-term investment growth.

How much could I get?

The earlier you start saving, the more your money can grow, and this really stacks up over time.

That’s because your pension isn’t just sitting in a bank account.

It’s invested, which means it has the chance to grow year after year.

This growth is powered by compound interest.

When you earn returns on your savings, these are reinvested.

Over time, this creates a snowball effect, and your pot gets bigger faster.

Even if you save just £100 a month from age 20 and stop contributing after 20 years, your pension could still be worth more than £200,000 at retirement.

That’s why starting early is so powerful.

2

What if I’m under 22 or earn less than £10k?

If you’re under 22 or earn less than £10,000 a year, you won’t be auto-enrolled, but you can still ask to join the company pension scheme.

Just speak to your manager or HR team and ask about voluntarily opting in.

If you earn more than £6,240, your employer must contribute to your pension, which means a chunk of free cash you wouldn’t get if you didn’t sign up.

Even if you earn less than that, you can still make contributions, and you’ll get at least 20% tax relief, which is essentially free cash from the government.

If you’re on a low starting salary, you won’t be paying huge amounts in, but starting early gives your savings more time to grow through compound interest.

It also gets you into the habit of saving regularly, which can make a huge difference later in life.

I started saving at 21 – I’m on track to have £805,991 when I retire

KATHERINE Wheatley started saving into a pension at age 21, while earning just £10,500 a year.

The 43 year old from London said: “My Dad always pushed the message that whatever you save into a pension in your twenties will be the saving that earns the most for you, no matter how small the amount was,” she says.

“When I started work I was earning about £10,500 and I really couldn’t spare a lot but managed to put aside about £50 a month and it built a habit.”

Now, that early pot is worth more than the contributions she’s made over the past 13 years, even though her salary is now five times higher than it was at age 25.

“This pot is the only reason my retirement forecast looks even slightly healthy, and I am so grateful for my Dad nagging me to do it.

Her advice for young savers? “Even if people don’t have a private pension to save in to, I really recommend the habit of saving small amounts – ideally that go out of your bank account on payday so that you never miss it.

“Whether it’s a pension or a holiday fund, or saving up for a rainy day, putting £50 away somewhere it’s out of mind builds up really fast.

“And for pensions, always try and contribute the maximum you can, as the employer rate will make so much more of it – particularly in your 20s, when that is free money.”

How employer matching works

Some employers offer more than the minimum contribution levels, which means you can save more, faster.

Typically, this works through something called matching, which means that if you’re willing to pay more, your employer will too.

Usually, you’ll have to choose to increase your contributions.

It’s well worth doing, because otherwise your company will keep the cash instead of investing it in your future.

For example, say your employer matches up to 8%, that means if you pay in an extra 5%, they’ll do the same.

Some companies even double match, meaning they’ll pay in twice what you do.

To find out what’s available in your workplace, check your employee handbook or speak to your HR team.

One great way to up contributions without it straining your budget is to wait till your next pay rise.

If you increase your pension contributions then, you’ll hardly notice the difference because you never had that extra money in your pocket in the first place.

Even increasing by just 1% or 2% could add tens of thousands of pounds to your pension pot over time.

How much should you save?

The legal minimum for workplace pension contributions is 8% of your salary, made up of 5% from you and 3% from your employer.

But experts agree this won’t be enough for most people to enjoy a comfortable retirement.

So how much will you actually need?

According to the PLSA’s Retirement Living Standards, a single person would need:

- £14,400 a year for a minimum lifestyle – covers essentials, with a little left over for fun.

- £23,300 a year for a moderate lifestyle – for more financial flexibility and things like an abroad holiday

- £37,300 a year for a comfortable lifestyle – includes some luxuries like regular travel and home upgrades

The full state pension is currently worth about £11,502 a year.

So, unless you plan to live very frugally, you’ll need your workplace pension to make up the rest.

There’s no hard and fast rule for what you should save, but some experts recommend aiming to pay in about 12–15% of your salary into your pension including your employer’s contributions.

I have a £200k pension – but I’ve not paid any money in for 13 years

KRIS Shergold began saving into a pension at 21, when he worked as an investment administrator.

The 46 year old from Streatham said: “At 21, you don’t know any different. I wasn’t earning a lot, probably less than £15k, but I was contributing somewhere between 5-8%.”

He says that the impact of this early saving on his retirement pot has been significant, accounting for around a third of his pension.

He can track the value because he started a new pension when he moved to a new job in his 30s.

When he consolidated his pensions into Hargreaves Lansdown in 2013, he was shocked. “I thought I had £30k… but it was £70k.

“Now it’s closer to £200k – and I haven’t contributed since I was about 33.

“It’s grown by 2 ½ times and I’m not even doing anything,” he said.

He adds that the early saving also gave him the expectation and discipline to always be saving into a pension, which has now translated into freedom to change careers in later life.

“It’s given me more flexibility at 47… knowing I’m projected to have a reasonable pension income regardless of what the future holds.”

He’s also passing those lessons on to his children.

“I’ve set up Junior SIPPs for my three daughters.

“A small amount invested today will compound to a huge amount in 60 years’ time.”

Tax relief: the government’s free top-up

One of the biggest benefits of saving into a pension is tax relief.

This is where the government adds extra money to your pension to reward you for saving.

If you’re a basic-rate taxpayer, the government adds 20% on top of whatever you put in.

That means a contribution of £80 becomes £100 in your pension.

If you’re a higher-rate taxpayer, you can claim up to 40% tax relief.

And if you’re an additional-rate taxpayer, the relief can be as much as 45%.

Higher earners may need to reclaim some of this tax relief through a self-assessment tax return, depending on how their scheme works.

But it’s worth doing, as that extra money can give your pension a significant boost.

5 tips to make the most of your pension

STEVEN Leigh – Associate Partner at Aon CAN WE GET A PIC OF STEVEN?

- The sooner you start, the better: Compound interest has been described as the eighth wonder of the world. The power of compounding is more impactful the more time it has to work its magic. Join your company pension as soon as you are able. The longer your money is invested, the more it will grow.

- Take full advantage of any employer contributions: Some employers will match your savings. If you save a little more a month, they may do the same – ‘free money’!

- Don’t try to do it all yourself: If you’re not an investment expert, then the pension ‘default fund’ will probably be the best place for your savings. The experts will be responsible for making sure your money works hard for you.

- Make up for lost time: If you miss any contributions because of absence from work (maternity/paternity leave, or caring for relatives, perhaps) try to make up it up if you can when you go back to your job.

- Saving more into a pension isn’t the best thing for absolutely everyone: Think about how much money you usually spend each month to help understand how much you might need to live on in retirement. The full state pension is currently worth around £1,000 per month. If you think you will need more than this, then saving more into a pension is probably a good idea. If you have any high interest loans or credit card debt, it’s usually wise to clear these as soon as you can before moving on to saving for your future. If in doubt, ask for advice – the Money and Pensions Service is a good place to start www.maps.org.uk/

Which companies offer the best pensions in the UK?

Public sector workers get final salary pensions, also known as defined benefit schemes.

These pay a guaranteed income for life, based on your salary and years of service – and are known as gold-plated pensions.

If you can get a job with a defined benefit pension, it gives you a significant advantage in terms of retirement savings.

Careers that come with final salary pensions include:

- NHS staff

- Teachers

- Civil servants

- Police officers

- Armed forces

Some private companies also offer excellent pension schemes, especially where employer matching is generous.

If you’re considering moving jobs, it’s always worth asking about your new employers’ pension scheme and whether matching is available.

You can also keep an eye out for other good benefits like funded financial advice.

Here are some examples of companies that offer over the minimum contribution rates:

- Unilever – Unilever employees get a reward package that includes a Benefits Envelope on top of pay. It’s worth 25% of pensionable earnings (basic pay and, for some people, other allowances). You can use it to save for pension, give yourself extra taxable pay or both.

- Shell – Shell UK employees receive a 20% total pension contribution, based on employee contribution of 5% via salary sacrifice and an employer contribution of 15%. As an optional benefit, total pension contributions can be increased to 27.5%, based on employee contribution of 7.5% via salary sacrifice and an employer contribution of 20%.

- HSBC – HSBC matches the amount employees put into their pensions up to a limit of 7% of monthly pensionable salary.

- Kingfisher – Offers a sliding matching scale. For employees who choose to contribute 8% or more, Kingfisher will pay 14% in.

- Legal & General – Legal & General’s contributions consist of both a ‘basic’ amount which is automatically paid and a ‘matching’ amount which is linked to how much employees put in. The maximum total contribution from L&G is 20%,

- Phoenix Group – Phoenix Group says it will match contributions up to 2% and will also enhance any Salary Sacrifice contributions made by 10%, that means employees could receive 14.2% whilst only contributing 2%.

- Royal Mail – In Royal Mail’s Collective Defined Contribution scheme employees pay 6% of pensionable pay and the company pays in 13.3%.

- Tesco – Matches pensions up to 7.5%

Changing jobs? Don’t lose track of your pension pots

EACH time you change jobs, you will be enrolled in a new pension scheme.

It’s easy to forget where all your old pots are, but it’s your money, and you can still access it.

The best thing to do is keep a list of all the pensions you have, and make sure you update the provider every time you move house, but if you haven’t, here’s what to do:

- Use the Pension Tracing Service to locate lost pots

- Keep a note of all pension providers as you move jobs

- Consider consolidating your pensions to make them easier to manage and reduce fees

However, there are times when it’s better not to combine.

Some older pensions come with valuable benefits, such as guaranteed annuity rates or lower retirement ages.

Before moving anything, check the terms, and consider speaking to an IFA.