THE minimum amount of money you need to live on in retirement each year has fallen – but there are ways of boosting your pot to get more.

Industry trade body The Pension and Lifetime Savings Association calculates how much a single person and a couple need to afford different levels of comfort in retirement.

1

They factor in all household bills, groceries, travel and car costs, going away on holiday, clothes, beauty treatments and more, into the amount of money you need per year.

There are three lifestyle levels – minimum, moderate and comfortable.

Here’s how much you need per year to afford them all.

How much do I need?

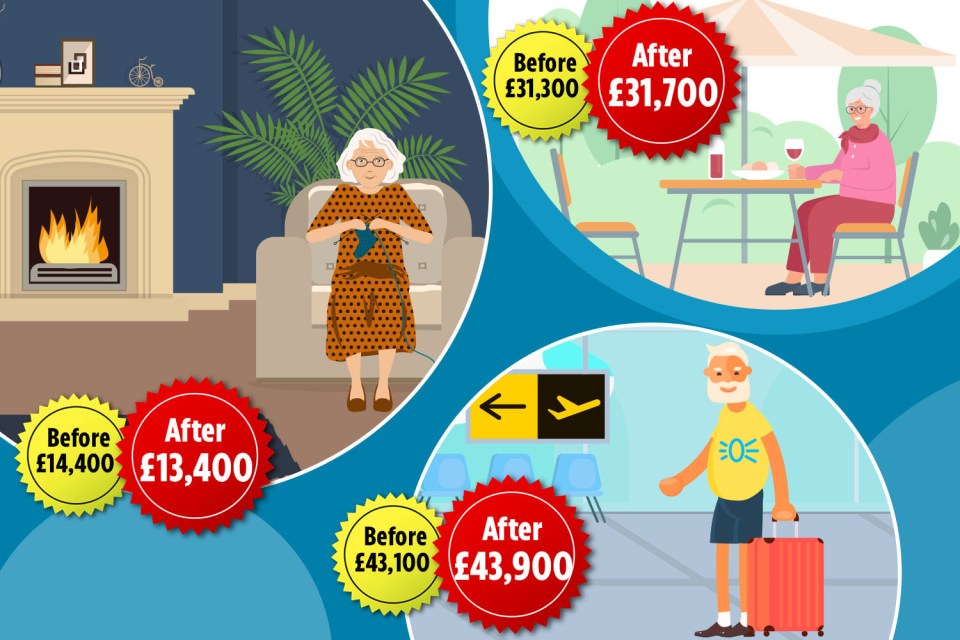

The amount of money you need for the most basic retirement lifestyle (a minimum retirement) has dropped.

A single person now needs £13,400, down £1,000 from £14,400, while a couple needs £21,600, down £800 from £22,400.

A minimum lifestyle covers all your basic needs, with a little bit left over for fun. This includes a small holiday and a cheap meal out once a month.

The PLSA said the amount of money you need per year for this lifestyle has gone down because of lower energy bills and a change in people’s expectations of the kind of lifestyle they can afford in retirement.

Meanwhile, the amount you need for a moderate or comfortable lifestyle in retirement has gone up.

For a moderate lifestyle, a single person would need £31,700, up by £400 from £31,300, while a couple would need £43,900, up by £800 from £43,100.

A moderate lifestyle includes one holiday abroad a year, eating out once a week, and budget for two or three weekly activities like going to the cinema or swimming.

For a comfortable lifestyle, a single person would need £43,900, up £800 from £43,100, and a two-person household would need £60,600 – £1,600 extra from £59,000.

A comfortable retirement includes a foreign holiday and several mini breaks a year, as well as beauty treatments and hair appointments every six weeks.

These calculations provide a guideline to help savers budget for later life, and to use as a measure to help keep on track with their retirement.

You may need more if you are still renting, or paying off your mortgage, in retirement. The PLSA said 17% of people expect to be homeowners with a mortgage or loan and 8% expect to be renting from a private landlord, according to its survey by 1,500 people.

The retirement living standard amounts were calculated by the Centre for Research in Social Policy at Loughborough University on behalf of the PLSA.

Tom Selby from AJ Bell said: “The good news for retirees is that the pain of rocketing inflation is now easing, which in turn is reflected in the drop in the cost of a ‘minimum’ retirement living standard.

“This is clearly a positive development although the nature of inflation means living costs for everyone, including retirees, will almost certainly be permanently higher in the future.”

SAVING FOR RETIREMENT

ANYONE planning their retirement needs to do some careful calculations about how much they will need to afford the lifestyle they want.

A good starting point is the government’s state pension age calculator, which will tell you when you will receive your state pension.

Visit gov.uk/state-pension-age to find out more.

Pension calculators can also help you determine how much money you need to save to have the pension pot you want at retirement.

The earlier you start saving, the easier it is as your money grows longer.

And you’re not on your own when saving for retirement.

Your workplace will almost certainly contribute some money to your pension pot, too, and you get tax relief from the government, which reduces the amount you have to pay yourself.

How you can boost your pot

It might feel daunting saving enough money to live on during retirement – but there are tricks to boost your pension pot.

A simple way to save more is to increase contributions into your workplace pension scheme.

Most people are now auto-enrolled into a workplace pension scheme.

A minimum of 8% of your salary must be paid into your pot – 3% will be paid by your employer, while 5% must be paid in by you.

It’s a really generous scheme, as in effect, you are getting free cash from your employer for your retirement.

The earlier you start saving into your pension, the longer your money has to grow, thanks to the effect of something called compound interest.

This means that over a long time frame, you could supersize your retirement pot.

Check your workplace pension scheme because some are more generous than others as some employers may match your contributions like-for-like.

Look into whether you can sign up to a salary sacrifice scheme, where you agree to take a pay cut and funnel this money into your pension instead.

This can be a great option if you are in danger of tipping over into a higher rate tax band. It’s a win-win situation, as your employer pays less in national insurance contributions too.

You may find that you have a missing pension pot if you have moved jobs.

Some £31.1 billion is lying in forgotten pots according to the Pensions Policy Institute.

You can use the government’s online Pension Tracing Service (or call 0800 731 0193) to help track down lost pensions.

It may be worth checking what your pension is invested in too.

There are roughly 14 million savers who have a defined contribution pension – where the money you get depends on how much you have saved, and how well your investments perform – in a “default” scheme.

A default scheme means that your investments are picked for your by your pension firm.

However, these are usually a “one-size fits all” plan which doesn’t take into account your personal circumstances, like your age.

When you are younger, you can generally afford to take on more risk with your investments, because you have time to ride out any dips in the market.

Meanwhile, someone approaching retirement may not want very low-risk options as their pension pot may not recover in time by the time they need it if their investments drop.

You can speak to a financial adviser about your options if you are not happy and thinking about switching out of a default fund.

STATE PENSION BASICS

AT the moment the new state pension is paid to both men and women from age 66 – but it’s due to rise to 67 by 2028 and 68 by 2046.

It is a recurring payment from the government most Brits start getting when they reach the state pension age.

However, not everyone gets the same amount, and you are awarded depending on your National Insurance record.

For most pensioners, it forms only part of their retirement income, as they could have other pots from a workplace pension, earning and savings.

The new state pension is based on people’s National Insurance records.

Workers must have 35 qualifying years of National Insurance to get the maximum amount of the new state pension.

You earn National Insurance qualifying years through work, or by getting credits, for instance when you are looking after children and claiming child benefit.

If you have gaps, you can top up your record by paying in voluntary National Insurance contributions.

To get the old, full basic state pension, you will need 30 years of contributions or credits.

You will need at least 10 years on your NI record to get any state pension.

The full rate of the new state pension is £221.20 a week – or £11,542 a year.

Under the old system, the full basic state pension is £169.50 per week and is paid to those who retired before April 6, 2016.

State pension payments are expected to rise by 4.1% in line with wages from April 2025.

This means someone on the full new state pension will see their payments rise by around £473 a year next spring.