Fears are mounting that the state pension age could rise faster as the government launches a formal review.

Ministers are reviving the Pensions Commission to find ways of heading off a crisis, with nearly half of Brits not putting anything into retirement funds.

However, at the same time reviews of the official pension age are kicking off examining the costs to the government and life expectancy.

Alarm has been sounded about the sustainability of the triple lock, which means the state’s old-age payouts rise by the highest out of inflation, earnings and 2.5 per cent every year.

The OBR watchdog warned earlier this month that the policy could cost three times as much as originally expected by the end of the decade, as the ageing population piles further pressure on public finances.

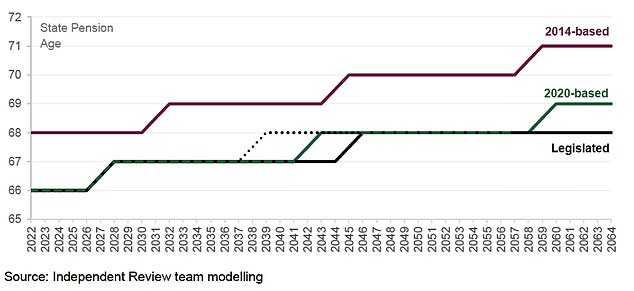

A government review published last March indicated that if life expectancy returned to the trajectory expected in 2014 the state pension age could be 71 by the late 2050s

The IFS highlighted that maintaining the state pension at current levels relative to earnings would mean increasing the proportion of GDP spent on it

Work and Pensions Secretary Liz Kendall said she was turning to the Pensions Commission, which last met in 2006, to ‘tackle the barriers that stop too many saving in the first place’

The pension age is already slated to rise to 67 between 2026 and 2028.

Currently the legal position is that it will reach 68 from 2044-46.

But a previous report by former Tesco director Baroness Neville-Rolfe cautioned that might need to be accelerated.

With the triple lock in place there are estimates the level would have to hit 74 by 2068–69 in order to maintain spending at around 6 per cent of GDP.

Lady Rolfe suggested setting a rule that Britons receive pensions for 31 per cent of the average life expectancy.

Those principles would have big implications for younger workers, with the Tory peer saying that the retirement age should reach 68 between 2041 and 2043.

It could then reach 69 between 2046 and 2048 – with those projections indicating that it would need to hit 70 in the early 2050s.

That would be when people born in the 1980s would be looking to bow out of the workplace.

Dr Suzy Morrissey has been commissioned to look at the ‘factors government should consider’ on state pension age.

And the Government Actuary’s Department has been asked to produce a report on the proportion of adult life in retirement.

The government says 45 per cent of working-age adults are putting nothing into their pensions.

Work and Pensions Secretary Liz Kendall said she was turning to the Pensions Commission, which last met in 2006, to ‘tackle the barriers that stop too many saving in the first place’.

The previous commission recommended automatically enrolling people in workplace pensions, which has seen the number of eligible employees saving rise from 55 per cent in 2012 to 88 per cent.

DWP analysis suggested 15million people were undersaving for retirement, with the self-employed, low paid and some ethnic minorities particularly affected.

Around three million self-employed people are said to be saving nothing for their retirement, while only a quarter of people on low pay in the private sector and the same proportion from Pakistani or Bangladeshi backgrounds are saving.

Women face a significant gender pensions gap, with those approaching retirement in line to receive barely half the income that men can expect.

The commission will be led by Baroness Jeannie Drake, a member of the previous commission, and report in 2027 with proposals that stretch beyond the next election.

But final decisions could be delayed until the next Parliament, despite concerns about giving people enough time to prepare for changes.

Laurence O’Brien, a Senior Research Economist at the IFS think-tank, said: ‘Despite the success of automatic enrolment in increasing the share of employees saving in a workplace pension, our recent research has shown that, among employees saving in a defined contribution pension, almost seven million appear on course for a disappointing income when they reach retirement.

‘Alongside this, only one in five self-employed workers are currently saving in a pension.

‘In the face of these trends, the launch of a new Pensions Commission, focusing on the adequacy of retirement incomes is welcome.

‘However, any reforms to boost pension saving must be carefully targeted to minimise falls in take-home pay among those who can least afford them.’