‘Up, up, up go the house prices.’ That was the TV news reporter’s opening line the first time I was invited to go on the television.

It was November 2006 and the reason that a much younger version of your correspondent had got ITV’s call to comment was that I had reported on a plan by a major lender to offer bumper mortgages.

Abbey, at the time the UK’s second biggest mortgage lender, had decided first-time buyers and home movers should be allowed to borrow up to five times their joint salary.

The early 2000s property market boom was about to hit its peak and an Abbey spokesman said: ‘Lending five times salary may sound high but really is something we have to do given what is happening with house prices.’

You can read the This is Money article on Abbey’s five times salary mortgages here.

It noted that while Abbey had made a fanfare about extending its lending, it wasn’t alone – some other banks and building societies including RBS and Cheltenham & Gloucester were also offering supersized loans.

We had written: ‘Some lenders go even higher – Northern Rock said its maximum loan was 5.9 times salary but added that it rarely allows borrowers to stretch that far.’

Almost 19 years later, the big financial news this week was that Chancellor Rachel Reeves is planning to allow mortgage borrowers to stretch that far.

Supersize me: Chancellor Rachel Reeves has decided banks should be able to issue more big mortgages at up to six times salary

Rules put in place to protect borrowers in the aftermath of the financial crisis will be swept aside to usher in a new era of bigger mortgages.

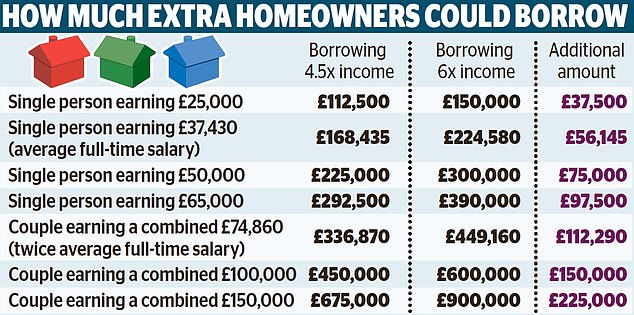

Banks and building societies will no longer be bound by rules that say only 15 per cent of their mortgage lending can be at more than 4.5 times income.

Instead, individuals and couples will be able to borrow up to six times their salary.

For a couple on a combined £80,000, this means potential borrowing would rise from £360,000 to £480,000.

Understandably, there are some deep concerns about the impact of allowing a pair of near average earners to take on an extra £120,000 of mortgage debt.

Put it this way, if you were in that position would you really want to take on a mortgage of almost £500,000?

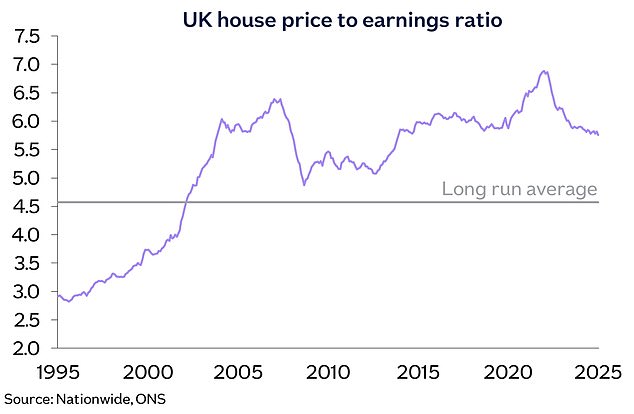

The ratio of house prices to earnings has fallen from its recent peak, as wages have risen faster than home values – but it remains far higher than the long-term average

Stretching your mortgage to the limit in this way dramatically increases the risk of discovering you have overextended your finances, particularly if you come off a fixed rate mortgage term at a time when interest rates have jumped.

First-time buyers and those moving up the property ladder also have a habit of discovering that the cost of running their new home comes in at more than they budgeted for.

Many of us who are lucky enough to be homeowners will have been there. You take an optimistic view of what your bills and running costs will be to justify thinking: ‘Yes, we can afford that home we really want’.

Reality bites about six months in. Something that was especially true for those of us who bought in the pandemic and then got whacked by bills soaring in the cost-of-living crisis.

When it comes to mortgages, we are in a very different financial world to 2006. It was a lot easier to borrow and overstretch back then and banks were eager to dish out interest-only loans.

The eagle-eyed will notice all the banking brands named above didn’t make it through the credit crunch-driven financial crisis that arrived in 2008. The banks that are around now are much more robust.

Meanwhile, the rules may say six times salary is possible, but that doesn’t mean you will get a mortgage that big.

Lenders assess now on affordability and if your incomings and outgoings don’t tick the boxes, they won’t lend you that much.

It’s also very easy to criticise this from both the comfortable position of being a homeowner and from a top-down zoomed out viewpoint.

Whereas, on an individual level, if a prospective borrower is already paying more per month in rent, then who can blame them for being very happy to take on a mortgage instead and at least be working towards owning the property.

Nonetheless, I can’t help but think this mortgage bonanza is a bad idea, as it will only serve to drive house prices up further.

You don’t need to be an economic genius to work out that if you lend people more money to buy homes, the price of homes will rise.

And this is unfortunate timing, as homes have got more affordable in recent years. The house price to earnings ratio has fallen from its pandemic boom peak, as wages have risen faster than home values.

Looked at from a broader perspective, homes are still very expensive though, at about 5.7 times earnings compared to the long-term average of 4.6. Albeit, this long-term average itself has been pulled up by the very high levels over the past 20 years.

Ideally, we need a prolonged period of wages rising faster than house prices to correct the market not a short-term fix of bunging people bigger mortgages,

Extending borrowing on the demand end also undermines the benefit of building more homes on the supply end.

I would argue too high house prices are a root cause of much of Britain’s economic ills over the past 20 years. Bumper mortgages only make things worse.