THE state pension is set to be boosted for millions and will rise to £12,548 from next year.

The increase of £574.60, which will come into force from April, was confirmed today.

The boost is due to the triple lock policy, which sees the state pension rise based on whichever is highest out of September inflation, average earnings growth between May and July, or 2.5%.

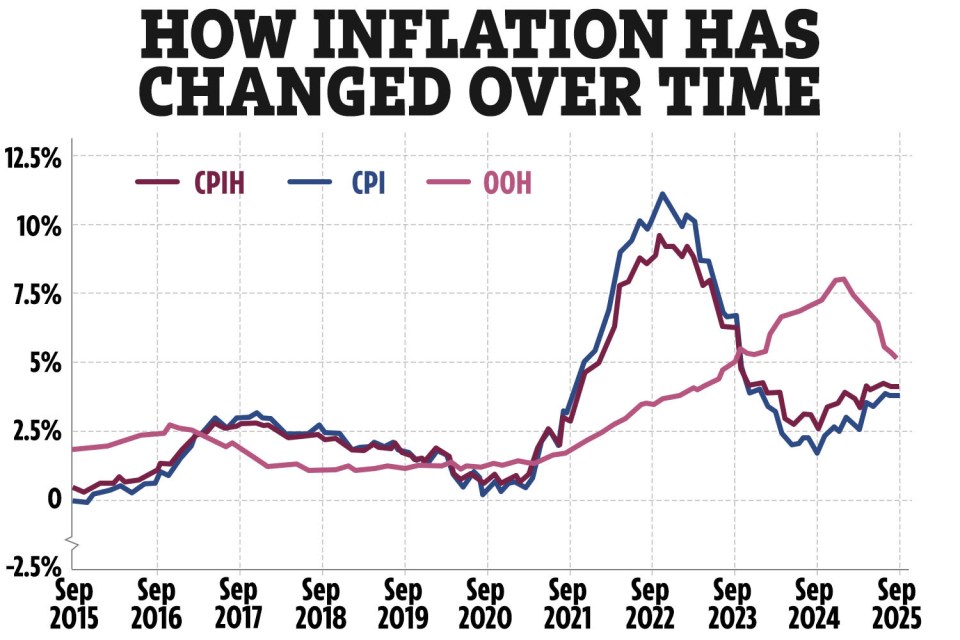

Inflation remained at 3.8% in September – the same as it was in July and August – the Official for National Statistics said on Wednesday.

This was lower than the earnings growth figure of 4.8%, meaning that pensions are expected to rise by this level from April next year.

While it will come as welcome news for retirees, it also means millions could be forced into paying tax on their state pension.

The personal allowance threshold, which is the amount you can earn before you start paying tax, is currently £12,570.

The rise in April will leave full state pensioners just £22 short of the threshold.

It means that millions could be forced to pay income tax on their pension when it rises again in the 2027/28 tax year.

Many more pensioners will also be dragged into paying tax on their savings from April 2026, if they have other savings on top of their state pension, such as a private pension.

Some 8.1 million people over the state pension age of 66 paid income tax in 2023-24.

But this could increase to 9.2 million by April 2026, according to estimates from the pension consultancy LCP.

There are also fears that the government will extend the freeze on income tax thresholds in the upcoming Budget, which are frozen until 2028.

This will also increase how many pensioners are dragged into paying income tax on their pensions as they continue to rise.

How much will your state pension rise by in April?

Anyone receiving the full “new” state pension will see it rise to £241.30 from £230.25 per week in April under the triple lock.

This applies to men born on or after April 6 1951, and women born on or after April 6 1953.

Pensioners born before these dates, meanwhile, will see their income rise from £176.45 per week to £184.90 per week.

Today’s news of the triple lock comes as the government is under increasing pressure to scrap the policy.

The measure costs the government huge sums each year, as Chancellor Rachel Reeves needs to find up to £30billion to plug the nation’s finances.

“The amount of money government spends on the state pension is already set to soar over the next few years, and the sustainability of the triple lock may once again come under scrutiny as a result of this latest bumper increase,” AJ Bell head of public policy Rachel Vahey said.

“If the triple lock sees the state pension increase above the personal allowance of £12,570 in April 2027, then the government will come under increasing pressure to either unfreeze the personal allowance or consider whether it can stand behind its promise to uphold the triple lock for the rest of this Parliament.”

How does the state pension work?

AT the moment the current state pension is paid to both men and women from age 66 – but it’s due to rise to 67 by 2028 and 68 by 2046.

The state pension is a recurring payment from the government most Brits start getting when they reach State Pension age.

But not everyone gets the same amount, and you are awarded depending on your National Insurance record.

For most pensioners, it forms only part of their retirement income, as they could have other pots from a workplace pension, earning and savings.

The new state pension is based on people’s National Insurance records.

Workers must have 35 qualifying years of National Insurance to get the maximum amount of the new state pension.

You earn National Insurance qualifying years through work, or by getting credits, for instance when you are looking after children and claiming child benefit.

If you have gaps, you can top up your record by paying in voluntary National Insurance contributions.

To get the old, full basic state pension, you will need 30 years of contributions or credits.

You will need at least 10 years on your NI record to get any state pension.