Analysts at investment bank Jefferies believe valuations for UK bank shares have ‘considerable scope’ to rise further in 2026.

In research this week, the investment bank pointed out that UK bank stocks comprised a large part of the FTSE 100‘s rally last year.

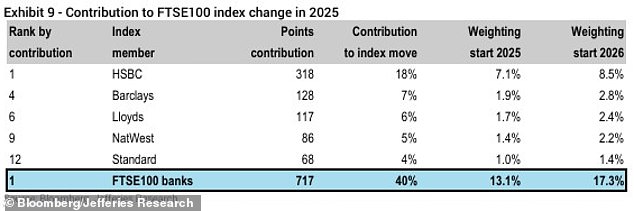

Britain’s banking sector accounted for 40 per cent of the FTSE 100’s points advance in 2025.

Asia-focused HSBC contributed 318 points to the 1,800-point increase of the FTSE 100 in 2025.

UK domestic banks, including the likes of Barclays and Lloyds Banking Group, delivered an 80 per cent total shareholder return in 2025, taking the aggregate over the last two years to 185 per cent – more than five-times the wider UK market.

On Tuesday, shares in Lloyds rose past 100p for the first time since the 2008 global financial crisis amid a wider rally in the London stock market’s blue-chips.

Gaining ground: Britain’s banking sector accounted for 40% of the FTSE 100’s points advance in 2025

Lloyds’ share price had not closed above the 100p mark since before the global financial crisis, where the bank’s shares plummeted from over 200p to lows of 44p in the space of 18 months.

Shares in Barclays have risen by more than 80 per cent in the last year, while NatWest Group shares hit a 52-week high on Tuesday.

‘Higher interest rates have been the key, allowing banks like HSBC, Lloyds, NatWest and Barclays to charge more on loans while keeping savings rates lower, which has boosted profits sharply’, Chris Beauchamp, an analyst at IG, told This is Money.

Some analysts think many UK stocks, including those of banks, are still trading at substantial discounts, offering savvy investors potential scope to enjoy bumper returns in the long-run.

Analysts at Jefferies this week said it was becoming increasingly challenging for underweight funds to ignore banks when their overall weighting has grown to 17 per cent of the FTSE 100.

It said most bank stocks were still trading at a discount of around 25 per cent compared to the wider market.

The investment bank added: ‘Indeed, that the banks trade on broadly the same two-year forward P/E multiple as the average since the financial crisis is remarkable, given the improvement in profitability and reduction in risk versus much of that period.

‘The simple passage of time may help rectify this, with every quarter of delivery adding support to the thesis that bank profits are more predictable and sustainable than in the past.’

Jefferies upped its price target on Barclays by 19 per cent to 560p, Lloyds by 13 per cent to 119p and NatWest by 14 per cent to 720p.

Amid a slew of buy recommendations, Jefferies’ analysts set Paragon Banking Group’s and OSB Group’s price targets at 1,060p and 740p respectively.

Jefferies said: ‘The days of making ‘easy’ money owning such stocks – where longer-term profitability considerations are arguably secondary – is largely over.

‘Investors looking to lift exposure to European banks may thus increasingly turn to shares on a low P/E. From a demand perspective, this bodes well for the UK banks.’

The investment bank said an upturn in fortunes at UK banks over the next few years looked set to stem from dividend and buyback estimates, rather than earnings.

In terms of potential risks for investors ploughing money into bank shares, as with any investment, shareholders could end up losing what they put in.

But Jefferies said the greatest risk to bank share investors remained a ‘major revision in interest rate expectations’. Faster cuts would hurt profits more quickly than expected.

It also flagged the potential impact of a change at the top of government, including the removal of Keir Starmer or Rachel Reeves, and an intensification of deposit market competition, driving tighter margins.

Contributions: A chart showing banks’ contribution to the FTSE 100 rally in 2025

What prompted the bank share rally?

Richard Hunter, head of markets at Interactive investor, told This is Money: ‘UK banks have had a generally stellar year, with the sector a strong contributor to the record-breaking success of the FTSE 100.

‘A sector rerating after years in the doldrums was a major factor.

‘Revenue tailwinds from the so-called ‘structural hedge’ (which effectively mitigates susceptibility to changes in a falling interest rate environment), lower than expected defaults and a return to deal making activity have all played a part.

‘In addition, the banks have all shown particularly sturdy balance sheets and their overall financial strength has enabled generous shareholder returns, both in terms of share buyback programmes and dividend payments.’

He added: ‘In terms of dividends, for example, in comparison to an average of 2.9 per cent within the FTSE 100, HSBC currently yields 4 per cent, NatWest 3.8 per cent, and Lloyds Banking 3.3 per cent.

‘Over the last year, each of the UK banks have enjoyed a formidable run, with the major beneficiaries being Standard Chartered, Lloyds Banking and Barclays, with gains of 83 per cent, 80 per cent and 79 per cent respectively.

‘In addition, NatWest and HSBC also made healthy progress with spikes of 61 per cent and 55 per cent.’

Hunter said potential blot on the landscape would be a deterioration of the economy in the UK or elsewhere, which could lead to an escalation of bad debts.

But he said: ‘However, to date there have been few signs of this becoming an issue and the banks have made adequate provisions to cover such an outcome.’

Updates: Jefferies has revised its forecasts for key UK bank shares

DIY INVESTING PLATFORMS

AJ Bell

AJ Bell

Easy investing and ready-made portfolios

Hargreaves Lansdown

Hargreaves Lansdown

Free fund dealing and investment ideas

interactive investor

interactive investor

Flat-fee investing from £4.99 per month

Freetrade

Freetrade

Investing Isa now free on basic plan

Trading 212

Trading 212

Free share dealing and no account fee

Affiliate links: If you take out a product This is Money may earn a commission. These deals are chosen by our editorial team, as we think they are worth highlighting. This does not affect our editorial independence.