House prices in Britain have risen by more than 6 per cent over the past year, official data revealed today as hotspots across the country were revealed.

The average property price is now £271,000, according to the latest House Price Index data for March 2025 which the Office for National Statistics released today.

Property prices increased by 1.1 per cent compared to February 2025 and by 6.4 per cent compared to March 2024 – a jump of £16,000 over the 12-month period.

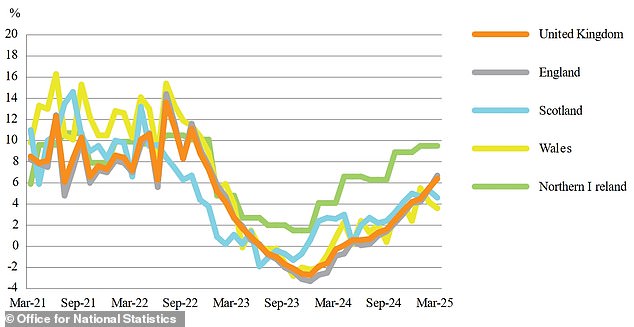

Values in the year to March 2025 increased in England to £296,000 (up 6.7 per cent), in Scotland to £186,000 (up 4.6 per cent) and in Wales to £208,000 (up 3.6 per cent).

Within England, the biggest winners were in the North East where prices increased by 14.3 per cent annually. But London saw the lowest value rise at just 0.8 per cent.

However London also had the two of the areas with the biggest monetary rise, with Redbridge up £45,000 and Lewisham up £42,000 – both equating to 9 per cent gains.

Sevenoaks in Kent also performed well over the year, up by £44,000 or 8 per cent; as did North East Derbyshire, also up £44,000 or 17 per cent; the Shetland Islands, up £42,000 or 18 per cent; and Rushcliffe in Nottinghamshire, up £41,000 or 12 per cent.

Completing the top ten were Havering (up £40,000 or 9 per cent), and then £39,000 rises for Mid Suffolk (12 per cent), Merton (6 per cent) and Mole Valley (7 per cent).

| AREA | ANNUAL % RISE | GAIN |

|---|---|---|

| 1. Redbridge | 9% | £44,807 |

| 2. Sevenoaks | 8% | £44,417 |

| 3. NE Derbyshire | 17% | £43,470 |

| 4. Lewisham | 9% | £42,011 |

| 5. Shetland Islands | 18% | £41,799 |

| 6. Rushcliffe | 12% | £40,822 |

| 7. Havering | 9% | £40,028 |

| 8. Mid Suffolk | 12% | £39,478 |

| 9. Merton | 6% | £39,329 |

| 10. Mole Valley | 7% | £38,703 |

| AREA | ANNUAL % FALL | LOSS |

|---|---|---|

| 1. City of Westminster | -20% | -£181,776 |

| 2. Kensington & C | -15% | -£179,444 |

| 3. City of London | -21% | -£148,722 |

| 4. Hammersmith & F | -13% | -£96,718 |

| 5. Islington | -8% | -£53,837 |

| 6. Camden | -5% | -£35,153 |

| 7. Cotswold | -7% | -£29,711 |

| 8. Newham | -6% | -£26,292 |

| 9. Inner London | -3% | -£18,513 |

| 10. Wandsworth | -2% | -£16,904 |

The change in average annual house price for the UK by country over the past five years

As for the biggest losers over the last year, nine of the top ten were in London – led by City of Westminster, which dropped £182,000 or 20 per cent in a year.

Kensington and Chelsea fell £179,000 or 15 per cent; then City of London dropped £149,000 or 21 per cent; and Hammersmith and Fulham slipped 13 per cent or £97,000.

Also having a bad year were Islington, down £54,000 or 8 per cent; Camden, down £35,000 or 5 per cent; Newham, down £26,000 or 6 per cent; Inner London, down £19,000 or 3 per cent; and Wandsworth, down £17,000.

The only area outside London in the top ten was the Cotswolds, down £30,000 or 7 per cent.

Tom Evans, sales director at Purplebricks estate agency, said: ‘House prices continuing to rise is great news for UK homeowners.

‘While the stamp duty changes that came into force from April 1 may not be felt quite yet, the prospect of more Bank of England base rate cuts will likely fuel demand and push up prices further this year – suggesting 2025 will be a strong year for the UK housing market.’

On May 8, the Bank of England cut interest rates from 4.25 per cent from 4.5 per cent – and Governor Andrew Bailey hinted more could follow over the coming months.

But the Office for National Statistics revealed today that Consumer Prices Index inflation had jumped to 3.5 per cent in April, up from 2.6 per cent in March and the highest since January 2024.

This two-bedroom first floor maisonette in Redbridge, East London, is on sale for £450,000

Buyers can get this one-bedroom flat in Sevenoaks, Kent, in a modern block for £350,000

This three-bedroom semi-detached house in North East Derbyshire is on sale for £250,000

Economists had been expecting a rise to 3.3 per cent last month.

Typically, high interest rates are used as a method to drag on spending demand and therefore bring down inflation – and today’s inflation figures may therefore see the Bank of England tread more cautiously with further cuts to interest rates.

Data from Moneyfacts shows the average two-year fixed mortgage deal is now 5.11 per cent – compared to a month ago when it was 5.23 per cent and a month earlier when it was 5.33 per cent.

The market has even seen some deals with rates of less than 4 per cent in recent months after a mini-price war broke out between mortgage providers.

Jonathan Handford, managing director of estate agent group Fine & Country, said: ‘March saw a final surge in house prices as buyers raced to beat April’s stamp duty changes, a deadline that drove a sharp uptick in activity and pushed values higher across the board.

‘This trend played out nationwide, with early 2025 marked by elevated demand from buyers keen to maximise their budgets before the new thresholds came into effect.

‘Now that the tax break window has closed, it’s likely we will see a cooling period, as buyers pause to reassess affordability under the revised rules.’

He said the two interest rate cuts from the Bank of England earlier this year had provided some relief by slightly easing borrowing costs and improving mortgage affordability.

But Mr Handford added that today’s inflation figures had ‘reintroduced some uncertainty’ and ‘may delay further rate cuts, keeping borrowing costs elevated for longer than previously hoped’.

He continued: ‘In the months ahead, inflation and still-elevated borrowing costs are likely to weigh on demand, particularly as affordability remains stretched across much of the country.

‘That said, a period of softer or stabilising house prices may offer a welcome opportunity for first-time buyers who have been priced out in some areas of the country.

‘Rather than a sharp correction, the outlook points to a more balanced market over the coming months, with modest price movements and cautious optimism as buyers and sellers adapt to the new landscape.’

Robert Nichols, managing director of Purplebricks Mortgages, added: ‘Rising house values coupled with falling mortgage rates is a big win for homeowners and would-be homeowners alike.

‘The bump in property prices should boost confidence in the benefits of investing in bricks and mortar while repeated Bank of England base rate cuts will spur both existing and prospective owners into making a move.

‘The downward trend in mortgage rates will fuel further interest in the market, meaning more for sale signs and more opportunities for that first foot on the ladder – making 2025 a great year for first-time buyers.’