Some circles of the British commentariat have perfected a peculiar ritual: that of prodding through good economic news, only to declare such news as bad. A major target for such investigation is Britain’s post-Brexit data. The latest data released by the Office for National Statistics quietly refutes the established narrative that “Brexit did deep damage to our economy”, as our Prime Minister said on 1st April. I promise you, it was not an April Fool’s joke.

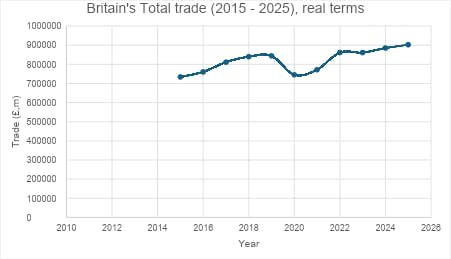

When measured in real terms, after Brexit total exports rose by more than 23 percent, from £735 billion in 2015 to £905 billion in 2025. Meanwhile, the fact that Britain’s trade has grown faster than GDP in the same period is an even sharper rebuttal of assertion by erstwhile Remainers that Brexit was an act of economic self-harm. These numbers are empirically robust, unarguable, and yet noticeably avoided in mainstream political discourse.

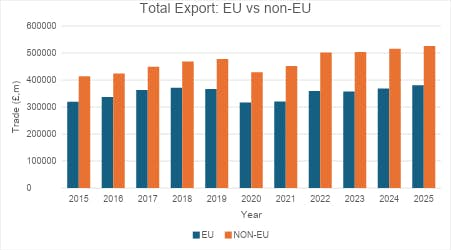

The aggregate value is impressive, but even more impressive is the growth composition. Despite Brexit taking several years to be actualised, and despite government failure to exploit its full potential, Britain has done a good job of optimising its restored trade sovereignty since the referendum. Since 2015, exports to non-EU countries have increased by 26.9 percent, with a 10.1 percent increase since 2019 (before the shocks of the pandemic and the TCA came into effect). In the same period, the share of Britain’s export to the EU has declined from 44.5 percent in 2014 to 41 percent lately. Yet rather than reflecting a worrisome loss of EU trade, this simply reflects Britain’s growing trade diversification beyond the EU.

In absolute terms, Britain’s trade volume with the EU has recovered and now surpasses its pre-Brexit trade volume in real terms. Although Britain has still increased its trade to the EU (growing by £380 billion since Brexit), the trade growth of £525 billion to non-EU countries makes for a more compelling story. This dynamic growth comes against the backdrop of shifting global trade as the EU bloc’s share of global GDP continues to decline. While Westminster conceives of every means to undermine Brexit, the British commercial landscape is expanding, one shipping container at a time, taking advantage of ascendant global opportunities and continuing to make the best of the EU despite its declining economic power.

Despite the growing prevalence of non-EU trade for Britain, our current Labour government continues to insist on the importance of “dynamic alignment” with various EU standards and regimes — that is, mirroring EU regulations onto British statute books whenever the EU changes them. Under dynamic alignment, Britain’s regulatory scope would be defined in offices it cannot enter and decided by parliamentarians not elected by the British people.

“Proximity demands conformity” is the premise of the argument for dynamic alignment. Given they are close neighbours, we are told we need to ensure trade being as frictionless as possible. After all, 41 percent of Britain’s exports is to the EU. A significant number, to be sure — but that means that 59 percent of Britain’s trade (and rising) is with non-EU countries. Locking-in Britain’s trade policy to that of 27 countries—all of whom are in direct competition against British exporters — risks sacrificing the diversification gained since Brexit for marginal gains in a trade relationship that was already recovering.

The dilemma the government faces has been made more complicated by the shock of the recent war in Iran. Since 28th February, when the US and Israeli military operations began, wholesale natural gas has almost doubled, and oil prices have surged past $100 per barrel. Furthermore, the OECD has given Britain its starkest growth downgrade: down from a previous forecast of 1.2 percent to 0.7 percent. Inflation, which was angling towards meeting the target rate of 2 percent, is now expected to climb up to 4 percent, with some economists speculating that it could reach 5 percent if the Strait of Hormuz remains closed throughout the summer. Since February, petrol and diesel prices have increased by 10 and 20 percent respectively. Haulers, manufacturers, and farmers are paying attention.

Britain’s oil security has been a cause for concern for a long time, as the Prosperity Institute reported in January. In January, GDP flatlined with the service sector recording no growth in the last quarter of 2025. The chief economist of WPI, Martin Beck, has warned that “with so little momentum heading into 2026, the economy is particularly vulnerable to the latest energy price shock”. Interest rates, which were expected to go down, may not be cut anytime soon. They may even increase.

Amid our turbulent economy, making wise decisions about trade is paramount. Contrary to the bleak prospects which doom-mongers had of Britain’s future post-Brexit, Britain’s export power has proven to be more durable than expected and more responsive to global demand than feared. Considering the sclerotic state of GDP growth, rising taxes and unemployment, Britain’s trade growth stands out despite weak domestic demand, as a success story that is only uncomfortable to those who doubt the dynamism of Britain’s private sector.

Dynamic alignment may be an attractive prospect, promising as it does some guarantees for ease of trade with the EU, and thus some sense of assurance in uncertain times. The government instead, should strive to ensure economic prosperity — a prospect still achievable with diversified global trade. As the ONS trade data shows, British trade with the EU is doing perfectly well without dynamic alignment. If anything, further deregulation across sectors would unleash manufacturing and farming which will further boost trade around the world. In light of the hard evidence, dynamic alignment is nothing more than misplaced ideological posturing and could spell doom for Britain’s trade sovereignty and make our already difficult economic situation even worse.