UP to 1.3million homeowners are facing shock mortgage bills following the outbreak of the Iran war, the Bank of England has warned.

Pressure is rising on UK households and the worst could be yet to come as borrowing costs continue to rocket amid the Middle East conflict.

Since the fighting started a month ago, the best remortgage rates from the top ten lenders have climbed from 3.77% to 5.01% on Wednesday, according to data from mortgage broker L&C.

This already adds around £140 extra a month – working out at £1,680 a year – to a typical £200,000 mortgage over 25 years.

But those hardest hit will be households rolling off older five-year deals, warned data site Moneyfacts.

These homes can expect average repayments to rise by between £417–£444 per month.

Adam French from data site Moneyfacts warned: “The real payment shock will be felt by those coming off older five-year deals, where rates have more than doubled, pushing up repayments by many hundreds of pounds per month.

“Unfortunately, anyone looking to buy or remortgage this year needs to prepare for substantially higher borrowing costs than expected before this conflict began.”

And experts fear these costs have not yet peaked, which could mean even more pounds added to bills for homeowners.

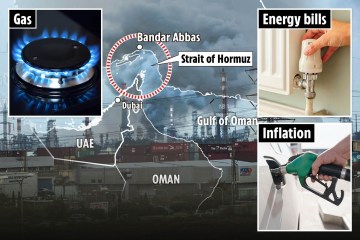

Oil and gas prices have surged since fighting began at the end of February, which feeds through to an increase in the cost of living.

The Bank of England typically raises interest rates when inflation rises.

The Bank’s latest financial stability report released this week warned UK households are set to face greater financial pressure due to increased energy prices and elevated mortgage rates.

Last month, the Bank’s monetary policy committee held the UK interest rate at 3.75% but financial markets are already predicting three interest rate hikes by the end of 2026 taking it up to 4.5%.

Interest rates translate to higher borrowing costs which is why lenders have already increased mortgage rates and pulled cheap deals from the market.

How high could rates go?

Now experts say the outcome for mortgage rates all depends on the war.

The expectation is for the market to remain volatile as lenders adjust to the changing picture.

David Hollingworth, associate director at broker L&C said: “How high rates could head will depend very much on the conflict and whether there can be an easing to the oil supply.

“Nonetheless I expect that borrowers need to expect more mortgage rate increases in the near term.

“There are still a number of deals below 5% but the lowest rates are increasingly edging nearer to and beyond 5%, especially for shorter term two-year rates.”

David predicts that if rates continue to rise like they have over the last month, the best rates will be around 5-5.5% with some deals pushing beyond 6%.

A £200,000 mortgage over 25 years on a rate of 6% would mean a monthly repayment £12,88.60 per month – that’s £258.16 a month more expensive than the beginning of March.

Over a year that would mean households scrambling to find an extra £3,097 a year to cover repayments.

Nicholas Mendes, mortgage technical manager at broker John Charcol added: “Nobody can say with confidence that we are at the peak yet.

“That is frustrating, but it is probably the fairest way to describe the market.

“Borrowers should be careful about assuming things will calm down neatly in the next week or two.”

Karen Noye, mortgage expert at financial advisers Quilter, agreed that if the war intensifies and the outlook for inflation soars further, we can expect to see rates climb higher.

She said: “Markets are now bracing for multiple Bank of England hikes in response to renewed inflation risk, even after a temporary easing in US military posture.

“A deeper conflict would harden those expectations.”

In this case, the mortgage market could be more more unpredictable and volatile with rates changing significantly within days.

On the other hand if the war ends, a rise in inflation could be just a blip.

Karen added: “Oil‑driven inflation has been the main obstacle, with markets reacting to supply fears pushing inflation expectations higher.

“If supply recovers, inflation should soften again, reducing the need for the Bank of England to follow through on the rate‑rise risk currently being priced in.

“Under that backdrop, mortgage rates over the next one to two years would likely resume a gentle downward path.

“We would not return to ultra‑low mortgage rates, but a drift back towards something nearer 4% becomes realistic.”

What to do if you’re planning to buy a home or remortgage

For anyone looking to remortgage or buy a home, securing a mortgage offer sooner rather than later is a good idea.

Mortgage offers can be valid for up to six months offering protection if rates increase further.

You can go ahead with the deal or search for a new offer if rates go back down.

Nicholas Mendes from John Charcol said: “For borrowers, the more useful focus is not trying to call the exact peak.

“It is understanding what can still be controlled.

“If you are remortgaging, waiting for total certainty can easily be the bigger risk. Many lenders allow borrowers to secure a new rate up to six months before their current deal expires.

“That gives you some protection if rates move higher again. And if pricing improves before completion, some lenders will let you switch to the better rate.

“In a market like this, having something lined up is usually better than waiting and hoping you catch the perfect moment.”