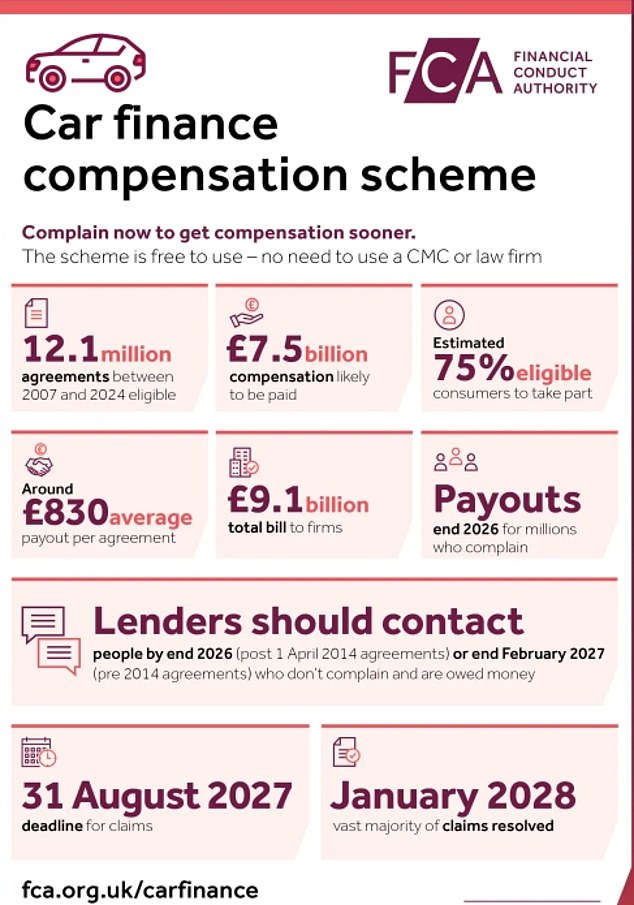

Millions of motorists will receive an average of £829 in compensation for rip-off car finance deals under plans announced today by the City watchdog.

The Financial Conduct Authority (FCA) said 12.1 million finance agreements made between 2007 and 2024 would be subject to the payouts as it revealed final details of the multi-billion pound scheme.

The number in line for cash has dropped from the FCA’s estimated 14million car finance agreements affected when its plan was first announced in October, but the average amount has climbed from £695.

Lenders have been lobbying the FCA to water down proposals for the scheme since they were first announced last year.

But others have said the planned payouts for consumers should be larger.

The total cost of the compensation is now expected to be £7.5billion, if 75 per cent of those affected make claims, lower than the previous £8.2billion estimate.

The FCA said ‘eligibility criteria have been tightened’ but average compensation has been increased for older agreements. Consumers have until the end of August 2027 to make a claim.

The watchdog will cap payouts in about a third of cases ‘to ensure no one is put in a better position than had they been treated fairly’.

Some have argued the pay-outs to consumers should be larger

Nikhil Rathi, chief executive of the FCA, said: ‘We’ve listened to feedback to make sure the scheme is fair for consumers and proportionate for firms. It will put £7.5 billion back into people’s pockets.

‘Now we need everyone to get behind it and ensure millions get their money this year. Payouts should not be delayed any longer, especially as household bills come under greater pressure.

‘Delivering compensation promptly also gives lenders the chance to rebuild trust, and means we can draw a line under the past and support a healthy motor finance market for the future.’

The scandal centres on the way car dealers were given commissions by lenders to sell loans to customers – and in some cases were given juicier pay-outs for flogging pricier finance packages.

The FCA boss last week told MPs on the Treasury select committee that its consultation – which was extended after lenders asked for more time – had received more than 1,000 responses.

Rathi said: ‘Much of it’s conflicting feedback because this is a dispute that’s been running for some time. It’s more likely than not that we will go ahead with the scheme.

‘We will consider all the evidence from all sides that’s been presented to us on all of the issues and then take a judgment in the round against our objectives.’

And Rathi defended the idea of setting up a scheme to deal with the scandal to avoid an extended and saga which could prove ‘very expensive’ and ‘run for many years’, while failing to provide timely compensation for consumers or certainty for investors.

The FCA has laid out its scheme and told people not use claims companies

The outcome was being closely watched by lenders who have already set aside billions to cover their estimated exposure to the compensation scheme.

Lloyds Banking Group has set aside £1.95bn, Santander has taken a £478m hit and Barclays says it is on the hook for £325m while smaller lender Close Brothers has made a £300m provision.

Today’s announcement came after the close of markets but the banks’ shares will be in the spotlight when trading resumes tomorrow.

Lenders have been critical of the scheme, with Lloyds saying it did not believe it ‘reflects the actual loss to the customer’.

And Close Brothers boss Mike Morgan recently told the Mail on Sunday: ‘You knew what you were paying for this car and you got the car. The customer got value throughout this.’

However, a group of MPs last week claimed that ‘drivers risk being short-changed’ by the FCA’s initial plans. They argued motorists should be receiving a typical £1,200 in compensation rather than £700.

Gary Greenwood, banking analyst at Shore Capital, said ahead of the announcement said the FCA needed to strike a fine balance.

‘Should the FCA proceed with its original proposals largely unchanged, we think there is a meaningful risk of a judicial review, which could delay implementation by a further 12–18 months’ he said.

‘Conversely, if the scheme is diluted too aggressively, there is a risk that claimants opt out of the FCA process and instead pursue lenders directly through the courts, often with the support of law firms or claims management companies.

‘While this route could result in higher individual payouts, up to a third of any compensation may be absorbed by adviser fees.

‘As such, the FCA faces a fine balance in designing a scheme that is both legally robust and attractive enough to drive broad participation.’