Hundreds of bereaved families are being hit with unexpected inheritance tax bills after falling foul of rules around making gifts.

Some 220 estates last year received a tax bill on £61 million worth of gifts given away incorrectly, according to HMRC data obtained by a Freedom of Information request by TWM Solicitors.

More families could unwittingly breach the rules and be hit with unwelcome charges as they try to avoid inheritance tax.

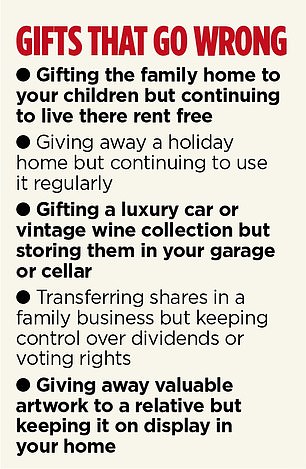

People making gifts slip up when they hand their loved ones assets, such as property, valuable artwork or fine wine, but still have use of them. This is known as Gifts with Reservation of Benefit – and the taxman treats them as if they have not been gifted at all.

For example, a parent might give the family home to a child, which can be done tax-free as long as they live for seven years afterwards. However, if the parent then continues to live in the property they must pay rent at the market rate, or it will be considered a Gift with Reservation of Benefit because they are continuing to use the asset as though it is their own. If they fail to do this, HMRC does not consider it to be a proper gift and, when they die, it will then be taxed as though it is still part of the estate.

Another example might be to give away a classic car, but then continue to keep it in your garage, or to gift a holiday home but still make use of it on a regular basis without paying a market rate.

Hit hard: Taxpayers paid a record £8.5 billion in inheritance tax in 2024-25 and £1.5 billion in the first two months of this tax year alone

Duncan Mitchell-Innes, partner at TWM Solicitors, says: ‘Making gifts is now one of the simplest ways of reducing an IHT bill, however many people are making mistakes in the process. Taxpayers should realise that simply handing over legal ownership of an asset isn’t enough to satisfy HMRC.’

Taxpayers paid a record £8.5 billion in inheritance tax in 2024-25 and £1.5 billion in the first two months of this tax year alone.

Currently about 5 per cent of estates are liable for inheritance tax but more are being caught in the net as the thresholds at which IHT kicks in remain frozen but inflation pushes up the value of investments, property and assets.

It is expected that the proportion of estates liable for IHT will rise to 8 per cent from 2027, when pensions are brought into the inheritance tax net. For many people, a pension is their most valuable asset, and this change in rules could tip them over the inheritance tax threshold.

Kirsty Stone, chartered financial planner at The Private Office, says: ‘We have seen a massive inflow of enquiries around inheritance tax and gifting since the pension changes were announced. ‘A lot of people might think that giving away their home seems like a quick fix, without realising the intricacies of the rules.’

Shane van Rossum, a retired school registrar, hoped to pass her pension pot to her daughter after she dies, but has had to change her plans since the Autumn Budget.

Since the announcement that pensions would be liable for inheritance tax, she has started taking regular amounts from her pot to reduce its value and mitigate any future inheritance tax bill.

‘I feel that I’ve worked hard to save money and I don’t want it all taken away,’ says Ms van Rossum, who retired ten years ago and lives in Fulham, west London. ‘I’m not trying to avoid inheritance tax, but I want to be savvy about what I do.’ She uses her annual £3,000 gifting allowance and also gives regular amounts to her family out of her surplus income.

‘I really did my research first and I make sure to keep accurate records of any gifts,’ she says. ‘If you want to leave money you need to be really sure about what you’re doing, and do your best to ensure that your family will get the best benefit from it.’

You can make gifts out of income that you don’t need so long as they are regular and come from income rather than assets.

DIY INVESTING PLATFORMS

AJ Bell

AJ Bell

Easy investing and ready-made portfolios

Hargreaves Lansdown

Hargreaves Lansdown

Free fund dealing and investment ideas

interactive investor

interactive investor

Flat-fee investing from £4.99 per month

InvestEngine

InvestEngine

Account and trading fee-free ETF investing

Trading 212

Trading 212

Free share dealing and no account fee

Affiliate links: If you take out a product This is Money may earn a commission. These deals are chosen by our editorial team, as we think they are worth highlighting. This does not affect our editorial independence.